Financial literacy is the capacity to comprehend and use a variety of financial abilities, such as investing, budgeting, and personal financial management.

Being financially educated empowers you with the necessary tools to manage your money wisely. This marks the beginning of a lifelong learning journey, where you take charge of your financial situation. Since education forms the bedrock of a secure financial future, the earlier you embark on this journey, the more in control you’ll feel.

Table of Contents

Toggle- ESSENTIAL NOTES

- Comprehending Financial Literacy

- The Pitfalls of Illiteracy

- Financial Literacy’s Range

- The Technological Evolution of Financial Education

- How Financial Literacy Is Improved by Technology?

- The Significance of Financial Literacy

- Essential Elements of a Financial Literate

- The Advantages of Having Financial Literacy

- Strategies for Increasing Financial Literacy

- An Illustration of Financial Literacy

- Conclusion

ESSENTIAL NOTES

- Knowing a range of crucial financial ideas and abilities is referred to as “financial literacy.”

- People who are knowledgeable about finance are often less susceptible to financial deception.

- A solid finance foundation may assist various life objectives, including managing debt responsibly, starting a company, and saving for retirement or school.

- Understanding how to make a budget, save for retirement, handle debt, and track personal expenses are all important components of financial literacy.

- One may acquire financial literacy by engaging with financial professionals, reading books, listening to podcasts, and subscribing to financial material.

Comprehending Financial Literacy

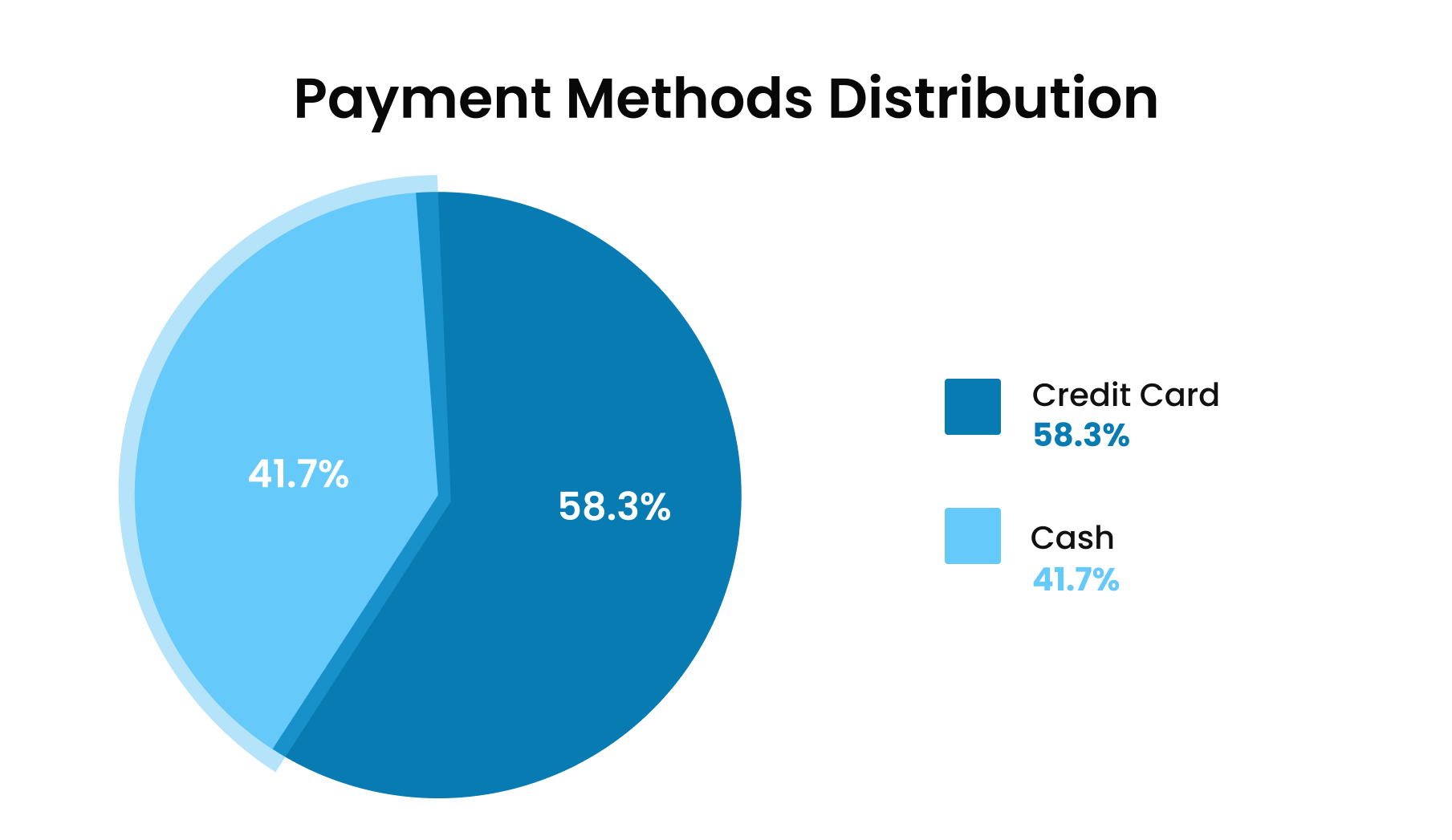

Financial services and goods have been more widely available in society since about 2000. While previous generations of Americans may have mostly paid with cash for their purchases, a variety of credit products, including credit and debit cards as well as electronic transfers, are widely used today. According to a Federal Reserve Bank of San Francisco poll from 2021, just 20% of payments were made using cash; 28% of all payments were made with credit cards.

Given the significance of money in contemporary culture, a lack of financial literacy may severely harm a person’s long-term financial performance.

The Pitfalls of Illiteracy

Financial illiteracy can lead to a host of risks, including the potential for unmanageable debt due to reckless spending or a lack of long-term planning. This could result in adverse outcomes such as bad credit, bankruptcy, home foreclosure, and other unfavorable situations. It’s crucial to be aware of these risks to avoid them.

Fortunately, people who want to learn more about financial matters have access to more resources than ever before. The Financial Literacy and Education Commission, an initiative of the U.S. government, is one such resource that provides several free educational opportunities.

Financial Literacy’s Range

Financial literacy may include a wide range of abilities. Still, typical examples include:

- Creating a family budget.

- Managing and paying off debt.

- Weighing the advantages and disadvantages of various credit and investment options.

These abilities often require at least a basic understanding of critical financial concepts like compound interest and time worth of money.

Financial literacy may cover both short- and long-term financial plans. Your age, investing horizon, and risk tolerance are some variables that will determine the method you choose. Understanding the future effects of your current investing selections on your tax obligations is another aspect of financial literacy.

The significance of financial goods has increased, including health insurance, school loans, mortgages, and self-directed investment vehicles, which are appropriate to utilize. At the same time, saving is also crucial, whether the aim is retirement or a financial objective like purchasing a house.

Other financial innovations, such as P2P lending, digital currency, and e-wallets, may be economical and practical, but their efficient usage depends on customers having the necessary knowledge.

Want to Hire Website developers for your Project ?

Let’s Discuss →The Technological Evolution of Financial Education

Financial literacy has become a dynamic arena where technology plays a vital role in the digital age, surpassing old limits. The merging of Fintech advances and digital banking has completely transformed how people interact with financial ideas, which has increased the effectiveness, accessibility, and engagement of personal finance education. This change is about a fundamental shift in how we perceive, engage with, and expand our financial knowledge, not only about how convenient it is to handle money using mobile applications or financial management tools.

The advent of online learning platforms, budgeting apps, and investment education materials has revolutionized financial literacy. These technological advancements have broken down the barriers that once hindered many from understanding financial concepts. Digital wallets, robo-advisors, and the gamification of finances have introduced a fresh, interactive approach to education that resonates with a generation that values instant gratification and online communication. The future of financial literacy is bright, thanks to these technological innovations.

It is imperative that we acknowledge the contribution of technology to improving our financial literacy even as we welcome these improvements. In order to ensure that people have a financially secure and technologically savvy future, this blog post will examine the various ways that technology is changing financial literacy, from FinTech innovations to the use of A.I. in financial education.

How Financial Literacy Is Improved by Technology?

It is indisputable that technology has the revolutionary ability to improve financial literacy. Fintech advancements in the digital era have changed how people and organizations approach financial education. Higher education institutions have found that integrating technology into financial literacy programs creates a more engaging learning environment and allows them to gather essential data on student engagement and learning results.

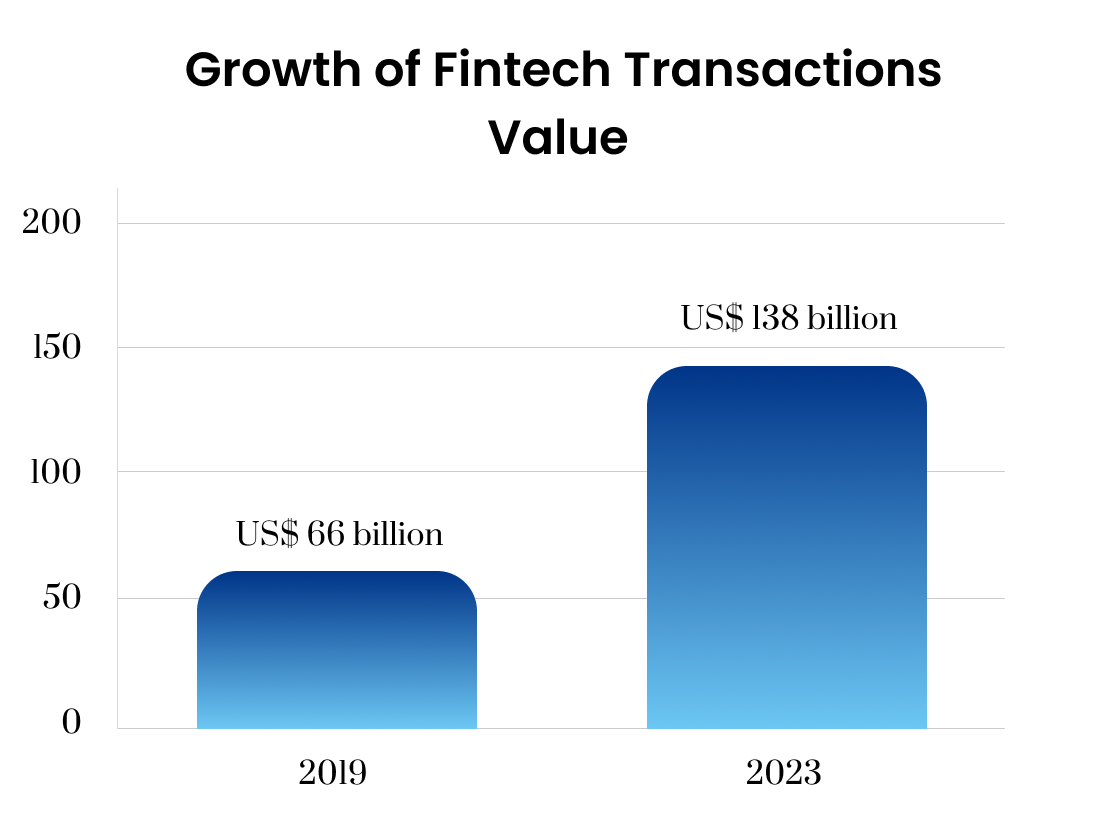

“The value of fintech transactions is expected to rise at a CAGR of 20% to US$ 138 billion in 2023 from US$ 66 billion in 2019.”

With digital platforms becoming an essential aspect of everyday life, technology significantly impacts financial literacy. These platforms provide a wealth of information and tools that may significantly enhance one’s understanding of finance and decision-making ability. Thanks to technology, financial education is now more participatory and accessible, ranging from smartphone applications that make saving and budgeting easier to online courses that cover intricate financial topics.

Putting digital first when it comes to personal financial planning is essential to using technology for financial literacy. This involves using digital experiences and resources that improve knowledge of financial management, from investing and budgeting to managing debt and retirement planning. A significant factor in this change toward a more technologically astute approach to finance is the use of Fintech, which is the term for the use of new technology to provide financial services more effectively.

Additionally, technology helps people of all ages, including young ones, become financially literate. Helping those who need it most, both personally and as a community, changes the game by making financial education not only more accessible but also more meaningful and effective. The introduction of digital currencies and safe online transactions to consumers has improved financial literacy with the emergence of blockchain technology, which provides a decentralized and secure mechanism for financial transactions.

The Significance of Financial Literacy

It Encourages Financial Security

Daily living costs, living within your means, short-term loans, and long-term financial planning forecasts. You need to be financially educated to handle these and other important financial realities throughout your life appropriately.

Budgeting and saving enough money to support a comfortable retirement while avoiding excessive debt that might lead to defaults, bankruptcy, and foreclosures is critical.

The U.S. reported on the “Economy Well-Being of U.S. Households in 2022.” The Board of Governors of the Federal Reserve System discovered that many Americans need to prepare for retirement. Of those who haven’t retired, around 31% thought their retirement funds were on track, while 28% said they had no retirement savings. About 63% of those with self-directed retirement funds acknowledged needing more trust in their ability to make retirement-related devices.

The Challenge of Millennials

According to a TIAA Institute study, millennials, who make up the majority of the American workforce, lack financial literacy, which has left them unprepared for a severe financial catastrophe. Only 19% of respondents, including those who claimed to have a high level of personal finance knowledge, correctly answered questions on basic economic concepts.

Forty-three percent of respondents said they had used pricey alternative financial services like pawnshops and payday loans. More than half did not have an emergency fund large enough to cover three months’ worth of costs, and 37 percent were classified as financially unstable if they could not or were not expected to be able to raise $2000 in a month in an emergency.

Millennials also have a high home and student loan debt. Indeed, 44% of them claimed to have excessive debt.

Despite the fact that they could seem to be personal issues, they affect the whole population more than was previously thought. Before the 2008 financial crisis, many people were unaware of mortgage products, which made them more susceptible to predatory lending. The crisis’s financial effects rippled across the economy.

The problem of financial literacy has wide-ranging effects on the state of the economy.

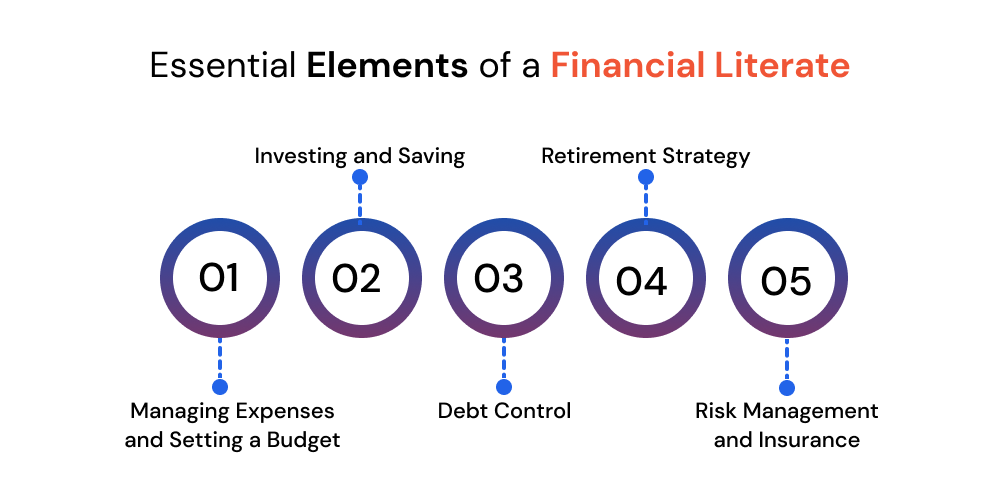

Essential Elements of a Financial Literate

Managing Expenses and Setting a Budget

To effectively manage your finances, you must have a clear grasp of your income and expenses, establish reasonable objectives, and keep an eye on your spending patterns.

Managing expenditures involves making deliberate choices to reduce unnecessary costs and prioritize those that are really required.

By being proficient in budgeting and cost control, you can save for future objectives, stay debt-free, and live within your means.

Investing and Saving

Setting away a part of your salary for future use is known as saving, and investing that money entails investing it in things or endeavors that may provide returns.

Upon registering, you will accept our privacy statement and terms of service. The Google Privacy Policy and Terms of Service are applicable, and reCAPTCHA safeguards Forbes.

Saving provides a safety net, but investing lets your money increase in value. Take advantage of diversification’s benefits and compounding consequences.

Debt Control

Financial education includes understanding how your credit score affects interest rates, being conversant with debt terminology, and formulating an effective payment plan.

It also involves knowing the difference between bad debt (like credit card bills for the newest iPhone, which is a luxury) and good debt (like education loans, which may be considered an investment in your future).

Retirement Strategy

Understanding Social Security and how deferring benefits might raise monthly payments, as well as pension plans, 401(k)s, and other retirement savings alternatives, is a necessary part of financial literacy.

Your intended retirement lifestyle, projected healthcare expenditures, and anticipated longevity are all taken into account in a thorough retirement plan.

Risk Management and Insurance

Various products, including property, vehicle, health, and life insurance, provide protection against different hazards. Make sure you have enough coverage for your particular situation.

Putting money aside for emergencies and increasing your nest egg are two more risk control techniques.

The Advantages of Having Financial Literacy

Financial literacy is generally advantageous since it enables people to make more informed economic choices. Furthermore:

Financial Literacy Can Prevent Devastating Financial Mistakes

While standard individual retirement account (IRA) contributions can only be withdrawn in retirement, floating-rate loans may have variable interest rates each month. Financial literacy may help avoid these costly monetary errors. Unaware of these and other financial truths, an individual may make innocuous financial mistakes that end up costing them money or altering their life goals. Those who are financially literate are better able to manage their own money.

Want to Mobile App Development for your Project ?

Contact Us →People Who Can Financially Literate Are Better Equipped To Handle Financial Difficulties

Subjects like emergency preparation and saving help people be ready for anything. Even while big, unforeseen expenses or job losses might have a negative financial effect, people can lessen the impact by consistently conserving money.

Financial Literacy May Assist People in Reaching Their Objectives

By developing a better grasp of budgeting and saving money, people can make plans that outline expectations, hold themselves responsible for their financial situation, and chart a path toward reaching significant financial objectives. Even if people can’t now afford their desires, they may still build a strategy to help them come true.

Confidence Stems from Financial Literacy

Picture yourself needing to make a significant financial choice without all the facts. People who are financially literate may make essential decisions in life with more assurance. They will be less likely to be taken aback or adversely affected by unanticipated events and have a higher chance of achieving the desired result.

Strategies for Increasing Financial Literacy

Learning and using techniques for managing and paying off debts, creating budgets, and other financial management tasks are all part of developing financial literacy. It entails being aware of and prudent with credit and investment items. The good news is that you can start adopting sound financial habits at any time, regardless of your current financial situation or stage of life.

Here are some doable tactics to think about.

Establish a Budget

Keep a record of the money you receive and spend each month. You may use budgeting software, paper, or an Excel spreadsheet. Income (checks, investments, alimony), fixed costs (least/rent, utilities, car payments), discretionary spending (non-essentials like dining out, shopping, and vacation), and savings should all be included in your budget.

First, Take Care of Yourself

This reverse budgeting method involves choosing a savings goal, such as paying for college, determining how much you want to put away each month, and setting that amount aside before you divide up the rest of your costs.

Pay Your Bills on Time

Keep track of your monthly expenses and ensure that your payments are issued and received on schedule. Aside from using bill-paying applications or automated debits from a bank account, think about setting up email, text, or phone reminders for your payments.

Obtain a Credit Report

Through the federally sponsored website AnnualCreditReport.com, users may get a free credit report once a year from each of the three main credit bureaus: Equifax, Experian, and TransUnion.

Examine these reports and dispute any discrepancies by contacting the credit bureau. Since you are eligible for three, spread out your requests throughout the year to monitor your credit.

According to a Federal Reserve study conducted in 2022, 27% of American respondents said they were not “doing okay” financially. From 2021.7, the proportion of those reporting a lack of comfort rose.

Verify Your Credit Rating

Among other advantages, having a high credit score makes it possible for you to get the most significant interest rates on credit cards and loans. Use a free credit monitoring service to keep an eye on your score. Alternatively, utilize a credit monitoring service if you can afford it and want to add an additional degree of safety for your data. Additionally, be mindful of factors like credit inquiries and credit usage ratios that may increase or decrease your ratings.

Control Your Debt

Utilize your budget to control debt by boosting payback and decreasing expenditure. Create a strategy to pay off your debt, such as first settling the loan with the highest interest rate. If you have too much debt, get in touch with your lenders to restructure your payments, combine your debts, or enroll in a debt counseling program.

Put Money into Your Future

Enroll in a 401(k) retirement savings plan your work offers and contribute the maximum amount to qualify for the employer match. Consider starting an IRA and building a varied investing portfolio, including commodities, fixed income, and equities. Consult with finance experts if necessary to ascertain the amount of money required for a comfortable retirement and devise plans to attain your objective.

Your Success, Our Priority

Turn Your Idea Into Reality

Talk to Us →

Talk to Us →

An Illustration of Financial Literacy

Emma is a high school teacher who uses her curriculum to try to educate her pupils about financial literacy. She teaches students the fundamentals of several financial subjects, including investing, insurance, tax planning, saving for education and retirement, managing debt, and personal budgeting. With the help of these principles, Emma’s pupils will be able to pay for enjoyable activities like going to the movies and things like renting an apartment or landing their first job.

Her kids may benefit from understanding ideas like budgeting, credit cards, bank accounts, interest rates, opportunity costs, debt management, and compound interest. These ideas also help them start saving and handle any student loans they may need to pay for their college education. It could prevent people from accumulating hazardous debt levels, jeopardizing their credit ratings.

In a similar vein, she anticipates that certain subjects, including income taxation and retirement planning, will ultimately prove helpful to every student, regardless of what they choose to do with their lives after high school.

Conclusion

Financial literacy is the capacity to make wise financial choices and the understanding of many facets of personal finance.

It entails creating a budget, figuring out how much savings is necessary, identifying advantageous loan conditions, comprehending factors that affect credit, and differentiating between investment choices that may be utilized to prepare for retirement.

Financial literacy equips people with the knowledge and abilities to manage their own money properly, safeguarding their economic prospects in the process.