The Fintech (financial technology) scene in India is on the brink of a transformative shift. Three key opportunities – the rise of digital payments, the expansion of digital lending, and the establishment of InsurTech – are driving this change. The Fintech sector in India has been on a steady growth trajectory, revolutionizing financial management practices for individuals and businesses through digital innovation. A recent analysis reveals a host of emerging prospects, including open banking, embedded finance, financial super apps, digital payments, digital lending, and insurtech, that have the potential to significantly reshape India’s Fintech ecosystem. Let’s delve into these exciting prospects and their possibilities for FinTech in India.

Table of Contents

Open Banking’s Ascent

Open banking, a banking practice where banks and non-banking financial organizations provide open access to customer banking, transaction, and other economic data to third-party financial service providers, is set to revolutionize the financial services industry. By fostering innovation, competition, and better client experiences, open banking can significantly expand the reach of financial services in India. Fintech companies, with their access to a wealth of data, can develop more specialized products and services, offer personalized guidance, and enhance risk assessment. Banks, on the other hand, can enhance their service offerings by leveraging innovations from third parties.

India’s open banking sector holds immense promise, provided it can navigate regulatory hurdles, ensure data security, and win over customers. Despite these challenges, the potential benefits of a more innovative and competitive banking sector make the future of open banking in India’s Fintech scene truly intriguing.

Integrated Financial Services via Embedded Finance

Incorporating financial services into non-financial platforms, applications, or services is known as embedded finance. Examples of embedded finance include social networking programs that facilitate peer-to-peer payments, e-commerce platforms that provide credit services, and ride-hailing apps that offer trip insurance.

Embedded finance, the integration of financial services into non-financial platforms, applications, or services, has the potential to enhance the accessibility, convenience, and efficiency of financial services. It can also open up new revenue streams for businesses and improve consumer satisfaction. With its rapidly growing digital economy and high mobile penetration rate, India is a fertile ground for embedded finance. The abundance of digital platforms across various industries, including healthcare and e-commerce, facilitates the integration of financial services.

Want to Hire Website developers for your Project ?

Super Apps for Finance: A One-Stop Shop

Another new development that has the potential to change India’s FinTech scene is the rise of financial super apps. A financial super app is a platform that provides a variety of financial services, such as banking, payments, investing, and insurance, under one roof.

Super applications are appealing because they are easy to use. By providing a single point of contact for all of their client’s financial requirements, they save them from having to use other platforms or applications. Super applications may help service organizations by boosting client engagement, making cross-selling easier, and offering insightful customer data.

Super applications for finance thrive in India because of the country’s high smartphone adoption rate and rising need for digital financial services. As more Indians go online to look for digital financial solutions, super applications may play a crucial role in India’s FinTech ecosystem.

The Increase in Online Payments

In India, digital payments are becoming more popular. Due to increased internet access and smartphone use, mobile payments are surging across the nation. Digital payments are now easier to use and more accessible because of the government’s goal for a paperless economy via the Unified Payment Interface (UPI). These days, digital payments cover more than just e-commerce transactions – they also cover regular utility bills, tuition for online courses, and even purchases from street vendors. Businesses are spearheading this change and making India one of the most prominent digital payment marketplaces globally.

Want to Mobile App Development for your Project ?

The Growth of Online Loans

The second considerable potential is digital lending, a field entirely transformed by cell phones and high-speed internet access. The advent of digital lending platforms has made conventional banking less sluggish and burdensome, offering speedier and more convenient options.

These platforms use technology to provide flexible repayment alternatives, minimum paperwork, reasonable interest rates, and speedy loan approval and distribution. This has made previously underserved populations, such as small enterprises and those without credit histories, more accessible to the credit market.

By creating creative solutions in response to changing company and consumer requirements, fintechs are actively changing the landscape of conventional financial services. The digital payments industry is a prime illustration of the changes they are bringing about since it is quickly adopting blockchain, artificial intelligence, machine learning, and the concept of a cashless society.

These businesses are expanding quickly due to their remarkable advancements, and investors are noticing them to capitalize on this positive trend. However, in addition to the potential rewards, there are many dangers associated with investing in projects related to the payment business. Discover the critical considerations for fintech investors by continuing to read!

Significant Prospects for the Contemporary Payment Sector

The following are some of the main elements that might make investment in the payment sector profitable:

Growing Interest in Online and Mobile Payments

Companies and customers were forced to resort to e-commerce during the COVID-19 epidemic to comply with the social distancing measures. Even in the wake of the epidemic, there is still an increasing desire for internet shopping. Indeed, it is anticipated that between 2020 and 2025, the worldwide digital payments industry will develop at a compound annual growth rate (CAGR) of 12.8%.

The need for digital payment solutions has increased due to the continuous rise in online sales. This presents investors with a significant chance to engage in a market poised for significant growth in the years to come.

Unrealized Potential in Emerging Markets

China, India, Brazil, Mexico, and other emerging nations provide enormous investment opportunities in the payments industry.

In many emerging markets, a significant portion of the population is underbanked or unbanked, lacking access to traditional banking services. Fintechs, by offering digital payment options that bypass the need for a traditional bank account, are playing a crucial role in promoting financial inclusion and bridging this economic divide. This underscores the transformative potential of Fintech in these markets.

Additionally, smartphone penetration is strong in many developing economies, hastening the acceptance of digital payment methods. In India, for example, smartphone penetration reached 71% in 2023 and is predicted to reach 96% by 2040.

Developments in Regulation

Global regulatory bodies are realizing the importance of digital transactions and are acting to facilitate their adoption and expansion. For instance, the Payment Services Directive 2 (PSD2) of the European Union, which came into effect in 2016, has long been influential in encouraging innovation and a healthy level of competition in the payment industry.

Furthermore, several nations are investigating the potential for implementing Central Bank Digital Currency (CBDC) and are establishing the necessary legal and regulatory structures for these initiatives. This involves discussing problems with the distribution, trade, insurance, and function of intermediaries of CBDCs.

Furthermore, several nations are investigating the potential for implementing Central Bank Digital Currency (CBDC) and are establishing the necessary legal and regulatory structures for these initiatives. This involves discussing problems with the distribution, trade, issuance, and function of CBDC intermediaries.

This is excellent news for investors wishing to enter this market, as these governmental actions foster the development of digital payment systems.

Hopeful Collaborations

Another encouraging trend is the growing number of partnerships between fintechs, established financial institutions, and technology companies. Through these agreements, innovators may increase the adoption of cutting-edge payment solutions while taking advantage of FIs’ extensive infrastructure and client base.

Recognizing the potential of these strategic alliances allows investors to remain ahead of the curve and profit from new trends that can influence the financial sector.

Principal Difficulties for Payment Businesses

As you can see, there is much opportunity in the payment sector. Before investing their money, however, investors also need to be aware of the difficulties this ever-changing industry poses. The following are some essential things to think about:

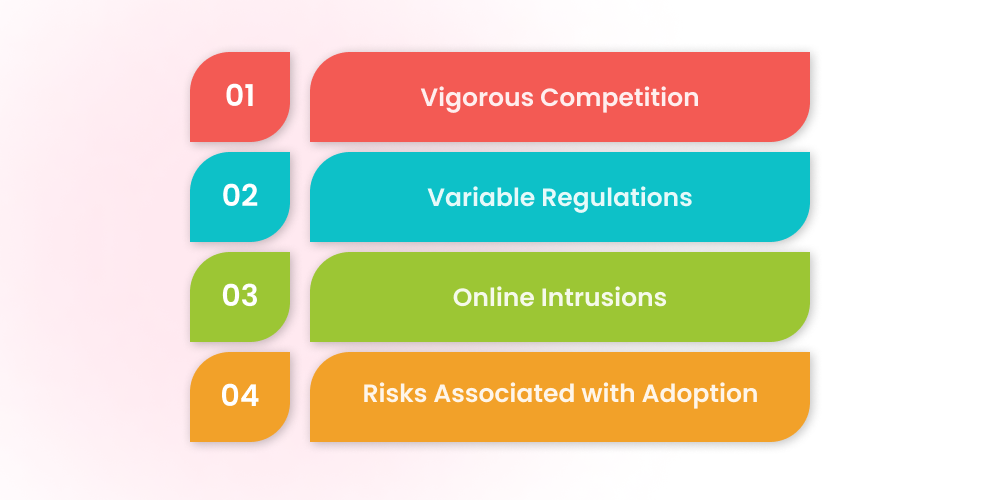

Vigorous Competition

In the very competitive payment sector, long-standing and more recent firms are fighting for market dominance. Due to fierce competition, it may be challenging for investors to allocate cash wisely.

Therefore, in-depth market research and a profound comprehension of distinctive value propositions are necessary to discern them and avoid choosing the incorrect opportunity. It is also essential to keep abreast of market trends and consult credible industry experts’ short—and long-term forecasts.

Variable Regulations

The financial sector’s regulatory environment is constantly changing, which may be advantageous and concerning. After all, it may be difficult for Fintech companies to maintain compliance because of the quick changes and regional variations in legislative requirements. Furthermore, as time passes, rules can get more stringent, which might restrict an organization’s ability to expand.

As a result, investors must keep up with the regulatory landscape in the areas they want to invest in and consider the potential roadblocks that may arise from any changes to the regulatory landscape.

Ready to bring your B2B portal or app idea to life?

Online Intrusions

Regretfully, hackers often attack finance firms. In 2022, for example, 1829 cyber incidents related to the banking sector were recorded globally.

Consequently, any security lapse may have severe repercussions for the company and its investors, such as:

- Reputational harm

- Clientele decline

- Disruptions to operations

- Data breach Expense Overruns

Therefore, before investing their money, investors must carefully evaluate the cybersecurity policies of the companies they want to work with.

Risks Associated with Adoption

Innovative digital payment solutions are in more demand than ever, yet it may still be difficult for new goods or technology to be adopted. Hence, investors need to assess the fintech companies’ chances of being adopted by the market. Among the crucial elements that need evaluation are:

- Usability

- Safety

- Pertinence to the issues faced by the intended audience

- Conformance with existing systems

- The payment solution is likely well received if every one of these elements seems promising.

Fintech Investing: Examining the Difficulties and Opportunities

Overall, the benefits of investing in the payment business will likely be the dangers involved most of the time. Investors in fintechs may anticipate significant returns on their investment with an emphasis on security and compliance, proactive innovation, and thorough market research.

But it’s crucial to always remember the industry’s difficulties and approach investing with caution and knowledge. Expert counsel is also beneficial, particularly if you are unfamiliar with the field or are handling large investment amounts.

Prospects for Fintech Enterprises

Sectors like commercial banks have a great chance to reconsider service delivery methods and determine how to take advantage of financial innovation. Numerous industries using Fintech’s cutting-edge solutions know its value and reap its benefits. Therefore, if your firm currently uses fintech services, take advantage of the favorable conditions to grow your business. The financial technology sector is expanding rapidly across many corporate landscapes.

Thanks to several current practices, the financial services sector can create more cutting-edge and inventive company solutions. In-depth study, report creation, corporate data analytics, and other strategies may be used to take advantage of the possibilities that might present themselves. Let’s discuss a few of the common approaches.

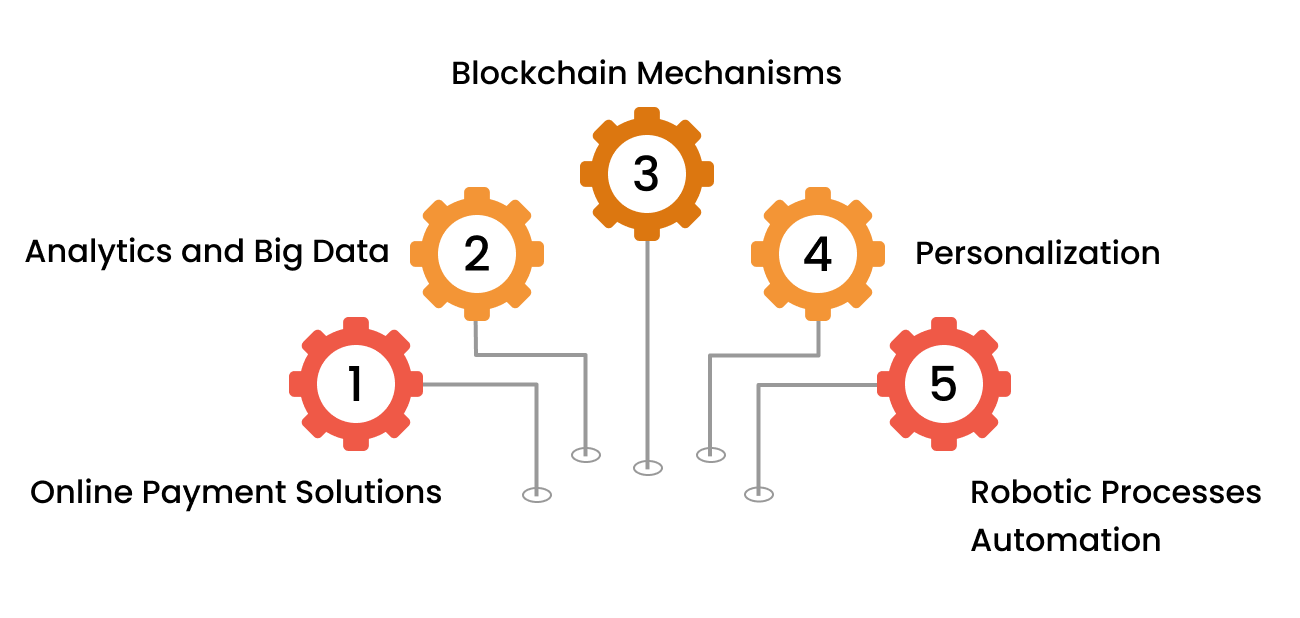

Online Payment Solutions

Digitalization is one of the typical revolutions that have occurred in many industries, including finance. Significant technical and structural changes are now taking place, and they are quickly taking on the characteristics of the new normal. Convenience and efficiency have increased with the emergence of digital-only banks. No one wants to visit the bank physically, stand in long lines, and complete a ton of paperwork. Digital-only banks allow you to create an account or make money, providing several great advantages, like bill payments, real-time analytics, and a quick overview of account balances and transaction histories.

Analytics and Big Data

Numerous financial organizations that compete in the market have been disrupted and transformed by digitalization in the financial industry. Data and analytics have advanced over the last few years, and as a consequence, organizations have grown to rely more and more on them.

Big data and analytics are widely used to generate more customized and targeted user experiences. Businesses use data and analytics to be competitive because they enable them to enhance operations, optimize revenue, anticipate customer needs, provide personalized product offerings, and estimate demand. Companies need to understand that analytics are available wherever extensive data is required. Their link is unbreakable. Businesses need to make a deliberate and comprehensive adjustment to these changes as the financial industry rapidly moves toward data-driven optimization. The business outcomes obtained from the gathered consumer data will be very informative.

Blockchain Mechanisms

Due to its quick adoption and growth, blockchain is quickly becoming vital to financial institutions’ operational infrastructure, including digital payments, stock trading, smart contracts, and identity management. Financial institutions are using blockchain more swiftly because of its speed, security, and global reach.

Fintech firms need to show transparency and build trust in their contracts and supply chains. Blockchain allows them to see visibility through the supply chain. It also manages performance benchmarking and quality assurance. Blockchain must be quickly incorporated into financial services systems, and they must look for opportunities to grow FinTech.

Personalization

Personalization and banking are two sides of the same coin. In banking, personalization is always advantageous to companies. Customization offers customers a worthwhile service or product based on historical data and personal experiences in the financial services industry. The pandemic now compels financial institutions to prioritize the necessities above the nice-to-haves. A customized partnership also promotes trust.

The primary driving forces behind the adoption of digital transformation are improved customer satisfaction and higher revenues. These days, financial institutions compete with one another and the biggest names in technology. To better understand its customers personally and adapt to the changing market, the financial services sector must reconsider its campaign measurement approach.

Robotic Processes Automation

Is there a banking procedure that you can think of that is both quick and efficient? That means you win this one. RPA has a track record of being among the most effective financial transaction management techniques. RPA may also refer to bots; thus, it’s only sometimes necessary to automate the process. The fact that RPA offers a superior user experience and affordable, intelligent wealth management advice undoubtedly contributes to its growth.

The need for virtual advisers is rising. People are anxiously awaiting sophisticated investment possibilities and in-depth market research to capitalize on the present circumstances. To capitalize on this unique potential, companies need to be ready to provide new products that include Robo advising services. Within the banking industry, they provide services, including customer service, account opening procedures, and other financial processes.

Difficulties Fintech Companies Face

There are various fundamental reasons why some organizations have not included fintech services in their operations. Either they lack startup service providers that can handle it or are unsure how to use Fintech—that information is acquired later. However, a few identified pain factors prevent other companies from using fintech solutions. A selection of them are listed below.

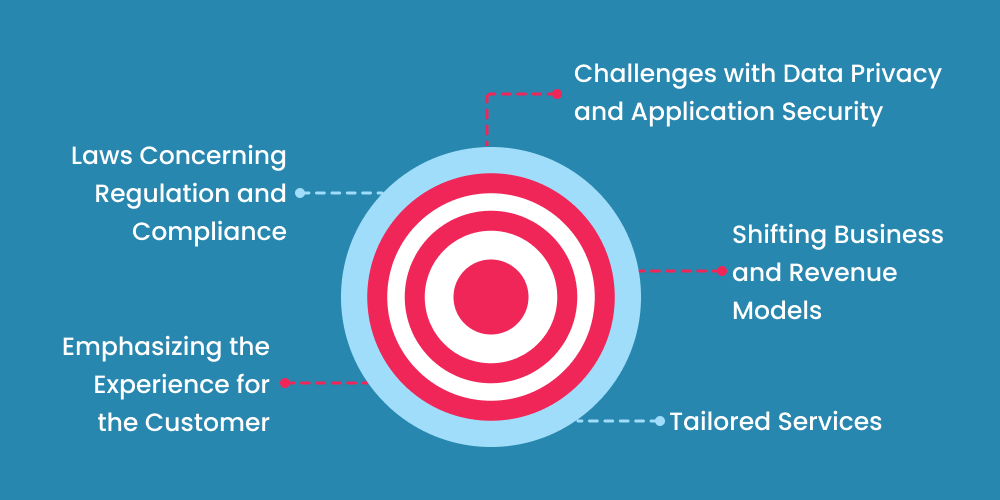

Challenges with Data Privacy and Application Security

Fintech companies keep a tonne of susceptible customer data due to the nature of their company, including social security numbers, credit card details, income and investment information, and more. This information is constantly in danger of being lost in transit due to the rise in the usage of phone and online banking services. Because of this, the information is susceptible. Therefore, risk is a constant concern regarding the application security and data privacy of fintechs. Information security is becoming more and more critical.

This is because technical improvements have enabled you to access essential IT infrastructure remotely. Complex data is more straightforward to impede financial data sources. The absence of physical checks on crucial infrastructure and endpoint devices transporting corporate data are further issues.

Laws Concerning Regulation and Compliance

Establishing a fintech company is complex. Getting permission to launch a fintech business has grown more challenging due to fraud warnings and data breaches. In addition to being difficult to follow, these regulations make it challenging for Fintech businesses to enter the Indian market. Compliance rules should serve as a strict foundation to prevent fraud. They also pose serious obstacles for nascent Fintech enterprises. Before they can start up, fintech startups have to fulfill many standards.

Emphasizing the Experience for the Customer

There is a perception that finance is complex. Despite this, fintech companies’ operating practices have rapidly evolved. Crafting an exceptional user experience that transcends a primary user interface still requires much work. Business innovation known as “conversational UI” focuses on a unique user interface that mimics chatting with a natural person. Users may get information from bots in the format that suits them best.

Fintechs have led the way in terms of accessibility and ease of use. Additionally, opening an account with any bank is now relatively easy. There is more openness when fees and levies are disclosed upfront. Trading platforms such as Robinhood have simplified financial terminology.

Shifting Business and Revenue Models

Fintech companies should reevaluate their approaches to revenue and expenses and modify or expand their resources. Many firms use cost-cutting strategies, such as staff layoffs and salary reductions, to deal with the economic crisis. If the company is successful, several adjustments must be implemented in enterprises. Changes in income sources and other business dependencies are included. Your business models will also change as a result. Fintech companies that handle contactless payments are repurposing their resources to handle increased transactions.

Tailored Services

As is well known, businesses need help to adapt and provide individualized services. Despite being the most essential banking component, companies need help to provide personalization. In today’s world, personalization means interacting with a user instantly via the channel of their choice. Clients understand customized services, and you must provide a solution designed to meet their needs. They are not prepared to make any additional concessions.

Additionally, consumers are open to accepting Fintech as a financial wellness advisor. A large number of choices might be overwhelming for many individuals. However, effective personalization guarantees that users only see relevant choices.

Conclusion

As we’ve seen throughout this blog on fintech prospects and difficulties, despite companies’ perceptions of industry issues, Fintech offers various benefits. However, if you choose the best partner for your financial requirements, obstacles may be overcome, and you can benefit. However, maintaining a balance between conventional banking practices and modern approaches is a challenge. Seek the advice of a fintech development business to maximize advantages.