Better money management has become necessary for many as a result of the COVID-19 epidemic. Banks and other financial institutions are giving their consumers additional tools in order to take advantage of this trend. However, what are the fundamental components of an efficient personal finance application?

An Economic Times report claims that COVID-19 has caused customers to become more frugal with their purchasing and more inclined to keep track of their expenditures. According to the report, over 76% of respondents in India and 62% of respondents globally said they had no alternative but to keep track of their expenses due to the financial impact of the epidemic.

Table of Contents

Toggle- The Significance of Managing One’s Own Finances

- The Need for an Application for Managing Personal Finances

- Personal Finance Topics

- Five Pointers for Handling Your Own Money

- How Can a Financial Plan Be Successfully Developed?

- Conclusion

Many individuals are jobless as a result of the COVID-19 lockdown and social distancing measures, which have severely damaged most sectors. As a result, people are now more aware of the benefits of sound financial management. Short-term financial difficulties have resulted from the pandemic-caused recession, but long-term consumer behavior changes should follow, particularly in personal finance. By building a solid relationship with their clients, financial services that recognize this impending change and provide their audiences with the appropriate information will be able to weather this catastrophe and come out stronger.

For this reason, having a deeper understanding of personal budget management is quite beneficial and vital.

The Significance of Managing One’s Own Finances

Financial planning, on a personal level, refers to carefully considered budgeting as a technique of allocating funds toward achieving life goals such as home ownership, retirement savings, kid education, etc.

Every aspect of one’s personal and professional life reflects the significance of personal financial management. No matter how wealthy or poor, everyone has to grasp personal finance management in order to maximize their assets and accomplish all of their future objectives.

According to a PwC Financial Wellness Survey, the leading financial worry is:

- The inability of Baby Boomers (52%) to retire voluntarily is a problem shared by Gen Xers (55%) and Millennials (62%), who lack sufficient emergency reserves for unforeseen costs.

Additionally, the poll reveals that:

- 49% of respondents said taking more work and household bills on schedule was difficult.

- 59% responded that their most significant source of stress is money or financial issues.

As its name suggests, an application for personal financial management is a tool for improved money management. It separates and combines a client’s financial data to provide a valuable outcome for improved financial planning. This program may assist with managing bank records, budgets, investments, portfolios, and other financial data by accepting a variety of financial data sources as inputs.

(Source: purrweb)

It’s essential to manage your funds for a number of reasons. The following are some of the strongest justifications for prudent financial planning:

Reaching Financial Objectives

Prudent money management may help one attain financial independence. Individuals who want to buy a house, pay off debt, or save for retirement may get closer to their goals faster if they have a plan and make informed choices.

Financial Stability

Those who manage their money well are more likely to be financially secure. Prudent cost monitoring, planning, and debt management techniques may help prevent overspending and debt growth, lessening their financial obligations and moving them toward financial stability.

Creating Wealth

With the right preparation and management, anyone can gradually enhance their net worth. By making wise investments, saving money, and managing debt, one can raise one’s net worth and become financially independent.

Making Defensible Choices

Making informed financial decisions is a crucial component of managing one’s finances. Understanding budgeting, saving, investing, and browsing may help people achieve their financial goals.

Preventing Financial Errors

Individuals who manage their own accounts often commit fewer errors in that domain. With diligent expense monitoring, planning, and debt management, one may prevent overspending, debt accumulation, and other financially disastrous mistakes.

Employing Cashless Techniques

Finance applications have revolutionized cashless transactions. When users can swiftly finish transactions by scanning their phones, they no longer need to look for ATMs. Because of the additional layer of protection provided by finance mobile applications, users’ financial information is protected against fraudulent transactions.

Convenient and Accessible Services

Banking applications allow users to get banking services from any location without visiting a physical branch. Your users now have the flexibility to handle their money whenever they choose, from the comfort of their home or on the road.

Setting and Adhering to a Budget

Because credit and debit balances are updated instantly, consumers can easily monitor their spending patterns. For added protection and peace of mind, most banks now enable customers to immediately deactivate their debit or credit cards via their smartphones if they misplace them.

Instant Money Transfer

Without the need for money orders or wire transfers, a user may send money to anybody, anywhere in the globe, with only a few clicks. For instance, Wells Fargo has mobile banking applications that make it simple to move money domestically and internationally while guaranteeing your security via authentication.

Understanding how to manage your personal finances is essential if you want to grow your wealth, be financially secure, and make wise financial decisions. It might help individuals become wealthier, reduce stress, and save money.

The Need for an Application for Managing Personal Finances

An application for managing personal finances helps in:

- Keeping track of income and spending to manage money

- Creating a budget and monitoring your savings

- Paying for different kinds of services

- Generating income from assets and savings

- Boosting cash flow with cautious budgeting, wise spending, and tax planning

- Providing for the financial stability of the family

- Verifying one’s credit score

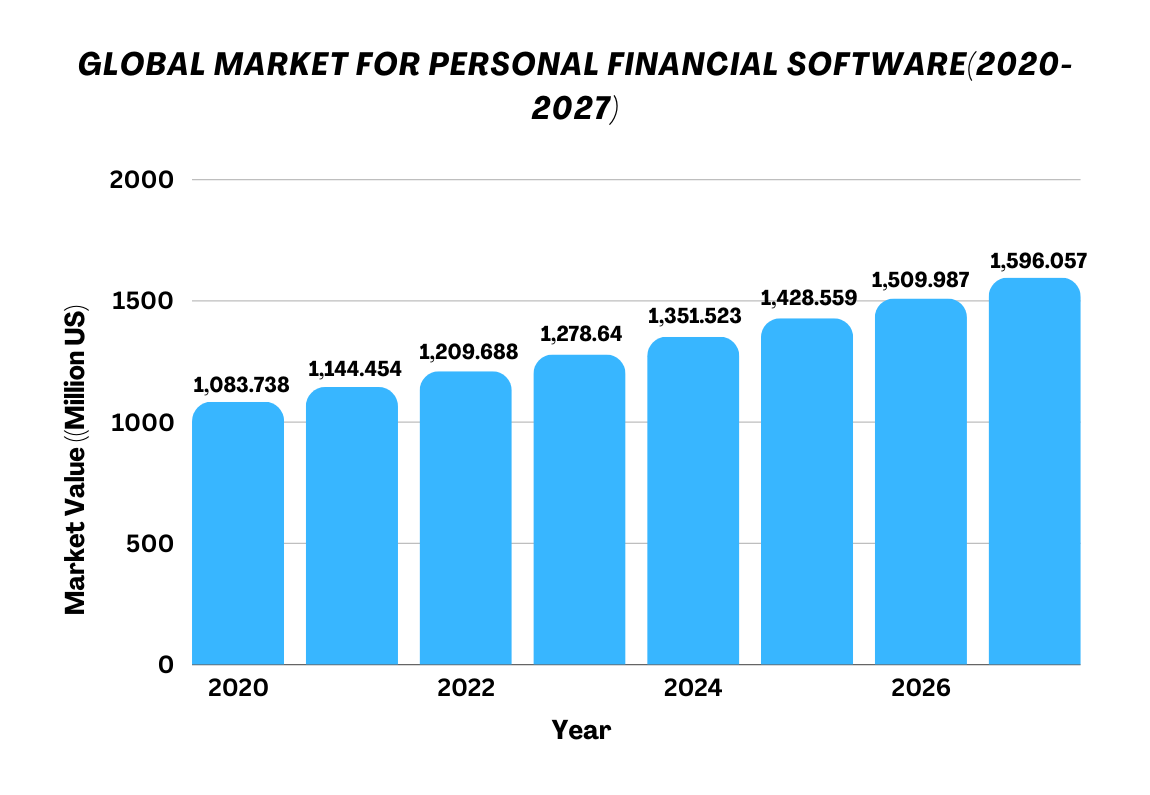

Allied Market Research estimated the global market for personal financial software to be worth $1,024.35 million in 2019. It is anticipated to increase at a compound annual growth rate (CAGR) of 5.7% from 2020 to 2027, reaching $1,576.86 million.

A study conducted by Attest found that the majority of people in the UK under 30 use personal finance apps. Most users utilize these applications once a week or every ten days on a monthly basis.

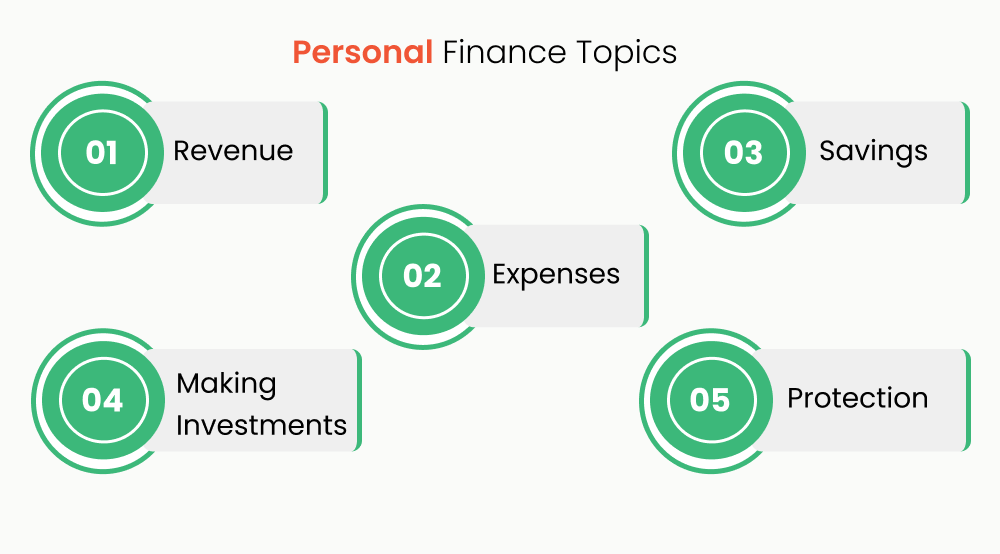

Personal Finance Topics

The five pillars of personal finance are protection, investing, saving, spending, and income.

Revenue

The foundation of personal finance is income. It is the total amount of money you get that you may use for spending, saving, investing, and safeguarding. Your whole revenue is what you bring in. This covers income from dividends, salary, and other sources.

Expenses

The majority of revenue usually leaves the house when it comes to spending. Whatever a person spends their salary to purchase is considered spending. Rent, mortgage, food, pastimes, dining out, home furnishings, house repairs, vacation, and entertainment all fall under this category.

One essential component of personal finance is effective expenditure management. People must ensure that their expenditures are lower than their income to avoid running out of money or getting into debt. Financial ruin may result from debt, especially given the excessive interest rate associated with credit cards.

Savings

The amount of money left over after expenses. Everyone should aim to have money to meet major bills or unexpected costs. That being said, it might be challenging not to spend your whole salary this way. No matter how hard it is, everyone should aim to have somewhere between three and twelve months’ worth of savings to cover any swings in income and expenditure.

Beyond that, money sitting around in a savings account is a waste, as inflation gradually reduces its buying value. Cash that isn’t needed for an emergency or spending account should be invested in something that will increase in value or held onto instead, such as stocks.

Making Investments

Buying assets—typically stocks and bonds—to generate a return on investment is known as investing. The goal of investing is to make a person wealthier than they started with. Since not all assets increase in value and might experience a loss, investing does include some risk.

It may be challenging for individuals who are not experienced with investing. It is helpful to set aside some time to learn about it through reading and research. If you lack the time, you may find it more advantageous to have a professional assist you with your financial investments.

Protection

The term “protection” describes individuals’ steps to safeguard their assets and shield themselves from unforeseen circumstances like sickness or accidents. Protection includes retirement and estate planning, as well as health and life insurance.

Five Pointers for Handling Your Own Money

Personal budget management doesn’t have to be complicated. With the appropriate strategy, you can take charge of your finances and move toward financial stability. Here are five valuable suggestions to help you get your money back on track.

Recognize Your Financial Objectives

Setting financial objectives is the first step to sound money management. These might be long-term intentions like retirement or short-term goals like saving for a trip. Knowing your objectives helps you prioritize where and how to spend your money and provides a clear path for financial choices.

Establish a Financial Plan

Creating a budget is one of the first steps to managing your money. This entails keeping track of your income and expenditures to understand your spending patterns. With a well-planned budget, you can better manage your spending, make sure you’re saving enough, and stay on track to reach your financial objectives.

Lower and Handle Debt

A significant barrier to reaching financial independence might be debt. Try to manage and reduce your debt, whether its loans, mortgages, or credit card amounts. One of the most critical stages in becoming debt-free is paying off high-interest bills first and avoiding needless borrowing.

Create an Account for Savings

Creating a savings account is an easy but efficient method of consistently saving money. Set aside a regular amount of your salary into an account that meets your requirements. This practice helps you save more money over time and prepares you for unexpected expenses and emergencies.

Employ Apps and Tools for Finance

In the modern digital era, many financial tools and applications may help you manage your money more easily. These tools may help with financial guidance, budgeting, managing costs, and monitoring assets. Using these tools may assist you in making well-informed choices and ease money management.

Your bank probably has a mobile app that provides various features to assist with budgeting, bill payment, and spending tracking. If you haven’t already, download the app and give it a try!

How Can a Financial Plan Be Successfully Developed?

Following your comprehension of the significance of personal finance, use these guidelines to develop an effective financial plan:

Establish Financial Objectives

First, decide on your objectives. Then, you can group them into short-, mid-, and long-term objectives.

Assemble Financial Information

Get pertinent data about the many kinds of savings and investment options on the market. This will assist you in weighing the benefits and drawbacks of each. Invest in line with your objectives and risk tolerance.

Establish an Emergency Fund

Ideally, this should include six to eight months’ worth of living costs. A fund like this may be utilized for emergency expenses like hospital stays, house improvements, etc. If you are unable to save a sizable corpus as an emergency fund, you may also take a personal loan to cover any emergency.

Look for Several Investing Opportunities

By considering your objectives and the economic data you have acquired, you may uncover various personal financial investment possibilities and allocate your funds appropriately.

Make both Long-Term and Short-Term Plans

You can monitor your progress and pursue your goals more efficiently if you divide your goals into short- and long-term financial plans.

Examine Your Plans

Make any necessary revisions to your plans and periodically review them to make sure you are moving in the proper direction.

With the aid of personal finance, you may build a financially secure future. Having a solid understanding of personal finance can benefit people in retirement and in monitoring their financial situation. It is important to remember that debt from personal loans is a crucial and strategic component of personal finance. Unexpected events could occur while implementing your financial plans, and you need quick access to money.

Conclusion

A firm understanding of saving, investing, establishing financial objectives, and creating a budget helps you become more accurate when dealing with money matters since they have many benefits. This perspective may help you organize, plan, and manage financial projects more precisely on a strategic level so that you may use this cunning financial strategy to increase your income. Your choice of level of comfort in life is directly impacted by how well you handle your finances. Whether you choose to spend money on luxuries or for temporary comfort is entirely up to you. Or choose long-term satisfaction via wise financial investments.