Table of Contents

Introduction

Brief Overview of the Greek Fintech Industry

Greece is well-known across Europe as a top vacation spot because of its year-round sunlight and turquoise waters. Nonetheless, the excellent pleasant climate of the nation contrasts sharply with the economic storms of the previous ten years. Thoughtful times are giving way to a new period of opportunity, and entrepreneurs are working to transform how Greeks handle their money entirely. Things are looking up, however.

Marqeta talked with the CEOs of Woli* and Finloup* and Antonis Prentzas and Marios Noutsos about how the Greek Fintech landscape is developing and what their companies want to accomplish in this recovering economy.

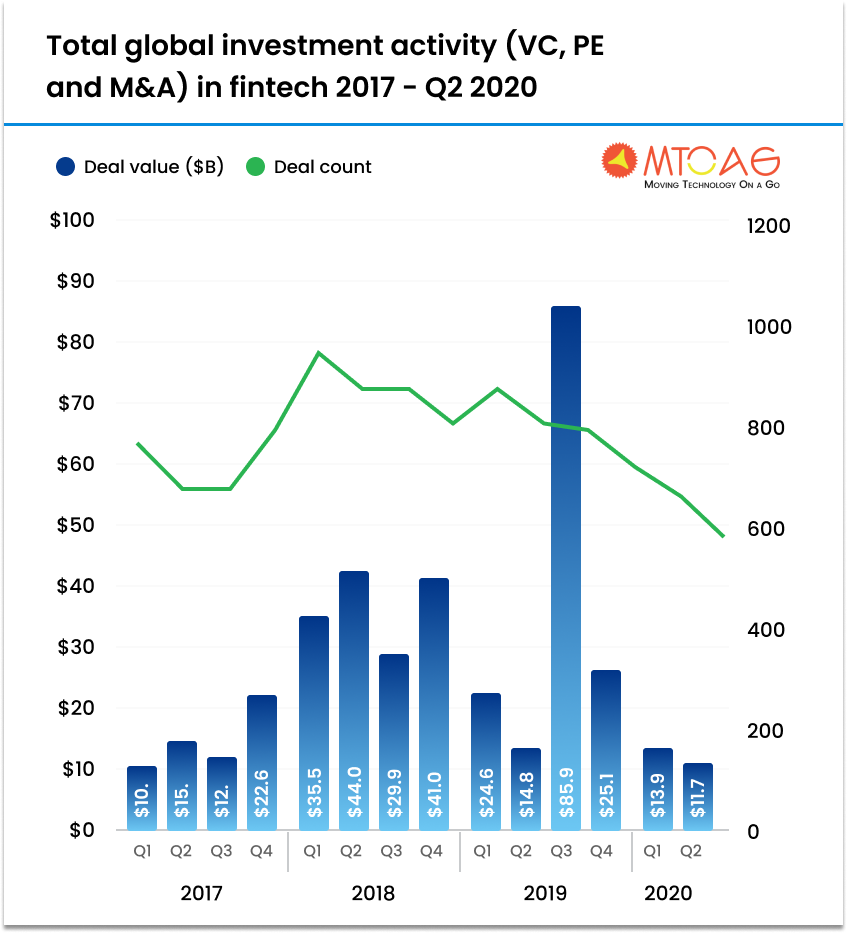

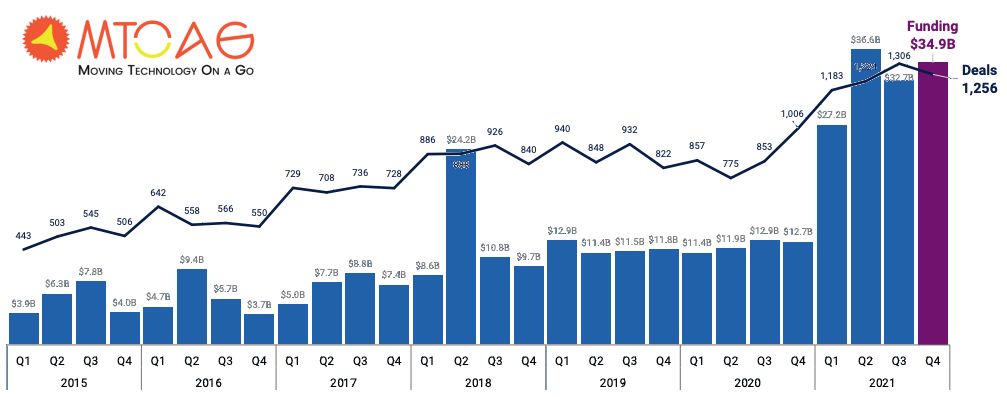

Payments-related investments were extremely robust in H1’22, totaling $43.6 billion, down from $60.3 billion for 2021. (Source: KPMG)

What Are You Doing to Foster Innovation in Greece?

Marios and Antonis: At Finloup, we are introducing buy now, pay later to the Greek market to assist people in equitably obtaining credit for modest, daily purchases by using only their debit cards. By collaborating with retailers, we can provide consumers with no fees and up to four monthly installments on investments, the finest of which is completed at the moment of sale. Also, depending on each customer’s income and history of consistent monthly payments for items like home bills, we employ algorithms to evaluate their capacity to repay. Without relying on conventional scoring techniques, which may not be as favorable to the application, this gives us a more trustworthy picture of a person’s creditworthiness.

Vasilis: Woli is a prepaid Mastercard app for kids and teenagers between the ages of 10 and 18, backed by an app under the supervision of a parent or legal guardian. With the help of the product, kids may keep track of their spending, receive insight into their behavior, and be paid to do tasks. The goal is to assist the next generation in developing financial literacy as they mature. We also participate in the area’s Central and Eastern Europe (“CEE”) innovation. Some incredibly intriguing fintech firms are emerging right now, and we have no doubt that some of these businesses will go global.

Finloup was also present at the event, Antonis and Marios, demonstrating that both Mastercard and Visa are actively seeking interesting businesses in Greece with which to partner. It’s a sign that innovation is gaining traction, and we’ll be looking to collaborate more closely with an extensive card programme shortly.

Greece received coverage in the international media throughout the 2010s due to its economic difficulties. How has the situation changed since then?

The nation had tough times with the implementation of capital restrictions in 2015. Several debts had to be written off, which impacted all of Greece’s central banks. There were enormous lines for ATMs and a withdrawal restriction of 60 euros. This had the unintended side effect of increasing card issuance since many customers bought more cards to enhance their withdrawal limits. Greeks always loved cash, but many now prefer cards.

Following lifting of capital restrictions, the government has promoted digital payments to increase economic openness. This included requiring retail establishments to install POS machines, leading to a dramatic rise in card acceptance. Only some companies are now excluded from accepting POS terminal card payments.

All of this indicates that the economy has started to quickly transition from a cash-based to a card-based economy due to the crisis and significant regulatory reforms. However, most cards are debit cards, with credit cards only accounting for 15% of the market. While we haven’t fully embraced ideas like “buy now, pay later,” I am confident it will happen soon.

Explanation of Fintech and Its Role in the Financial Industry

Businesses are developing cutting-edge strategies to accomplish their objectives with the assistance of a fintech consultant as technological maturity is at an all-time high. One of them also consists of financial solutions. It is a process wherein advancements in the banking, insurance, or other financial services sector have given rise to new technologies and have made it feasible for customers to trade with businesses more affordably, quickly, and effectively. It is a revolution that introduces new services and goods to alter how things operate. You may depend on financial technology consultancy for extra assistance with this.

What, then, is the key to this robust industry? Let’s look at the main arguments for the importance of fintech.

1. The Financial Technology Revolution Aids in Improving the Economy.

Fintech has developed and changed the financial industry in the most significant conceivable ways. Not to be overlooked is that a number of financial-related sectors are converting from manual to digital processes with financial planning software. In addition, the industry has quickly adopted e-wallets, mobile banking, digital payment, and paperless financials because of technological improvements.

2. Fintech Is a More Affordable Option

Traditional banking and fintech are often contrasted, and it is frequently observed that fintech businesses provide premium services at a reasonable cost. Due to the lack of physical branches, some banks allow you to retain more money in your pocket by waiving the account opening cost. Fintech companies also use technology and its potential to automate various tasks. By doing this, they save money on labor expenses.

3. Fintech is shaping the Financial Sector Of Today.

Banks predominated the financial industry in the past, but things have changed in the banking industry nowadays. Financial institutions are experiencing a loss in earnings, poor productivity, and several other setbacks. On the other hand, many financial industries only make modest development owing to inadequate banking infrastructure and ineffective I.T. systems. Hence, digital banking has transformed banking software services by drastically cutting transaction costs and simplifying procedures.

Thesis statement: In this blog post, we will explore how fintech mobile apps disrupt the financial industry in Greece and how companies can benefit from them.

Greece’s financial sector has been upended by fintech mobile applications, which provide creative solutions that are easier to use, more effective, and less expensive than conventional banking techniques. Digital banking, payments, investments, and customer experience are a few of them. Fintech mobile applications may help businesses by enhancing the customer experience, boosting productivity, and opening up new markets. Users of digital banking may create bank accounts, send money to others, pay bills, and manage their finances using their cellphones. Compared to conventional payment methods, payments are cheaper, quicker, and more secure. Investments in stocks, bonds, and other financial instruments are simpler to make.

The Role of Technology in Fintech

Explanation of How Technology Is Driving Fintech Innovation

Many businesses’ bank-end support functions used to be handled by financial technology. Venture investors seldom invest in the industry since they need to recognize its significance. Everything has changed during the last ten years, as venture capital has exploded and investments have gone from 5% to 20%. The fintech sector now exists in the innovation economy. Global banks established corporate venture arms and digital incubators as fintech expanded, investing in, acquiring, and enhancing startup companies’ offerings. We are at the intersection of the second wave of disruption in fintech, which Zaggle describes as a true game changer.

Personal finance is far less complicated than business financing, a nuisance many businesses outsource to professionals since they must deal with bank deposits, interest rates, corporate investment, lenders and creditors, and debtors. Corporations have had many difficulties managing office budgets since managing the external environment is their crucial competency.

Throughout the whole value chain, digitization is taking place. Cell phones are replacing face-to-face encounters in front-of-house connections. Assessment, onboarding, and customer service processes are all becoming automated. Due to this automation, there is intense vertical rivalry across diverse industrial sectors as they change course to package and cross-sell their services. Banks and digital payment applications have teamed up to provide customers with simple lending and payment choices.

In the last ten years, product-led solutions have shown to be more advantageous to corporations. Zaggle Save, cost management, helps your companies to spend more wisely and makes it possible for them to become cashless and paperless. All employee spending can be readily tracked, and data can be synced to accounting systems.

82% of financial services executives say that fintech is a strategic priority for their company. (Source: PwC)

Examples of fintech technologies (e.g., blockchain, A.I., mobile apps)

- Artificial Intelligence (A.I.): A.I. tools like machine learning and natural language processing are being utilized to streamline financial operations, enhance fraud detection, and provide individualized financial guidance. The banking sector likewise uses chatbots and virtual assistants more often to help clients and support them around the clock.

- Blockchain: New categories of financial products, such as cryptocurrencies and smart contracts, are being developed using blockchain technology. Systems built on the blockchain provide more security and transparency than conventional economic systems and may facilitate quicker and less expensive transactions.

- Mobile Devices: Smartphones and tablets have transformed how customers engage with financial services thanks to mobile technology. Users of mobile banking applications may access their accounts from any location at any time to check their balances, transfer funds, and make payments. This has improved banking for millions of individuals worldwide by making it more manageable and accessible. Mobile banking usage has grown by 50% globally since 2017. (Source: Marketing charts)

Benefits of using technology in finance (e.g., speed, convenience, accuracy)

Any particular law does not cover the advantages of using technology in the banking industry. These are some instances of how technology might help the financial sector instead:

Speed

Thanks to technology, financial transactions can now be performed more quickly than conventional techniques. For instance, clients may instantaneously move money between accounts using Internet banking, but a paper check may take several days to process.

Convenience

Regardless of a person’s location or schedule, technology makes financial services more readily available. Customers may manage their accounts on the move using mobile banking applications instead of going to a bank location.

Accuracy

Technology may assist in lowering transactional mistakes. Automation lowers the possibility of errors since it can execute computations and check considerably more precisely than people.

Benefits of Fintech Mobile Apps for Companies

Improved Efficiency and Cost Savings

One of the main advantages of developing fintech apps for organizations and developers is cost savings. Fintech applications are built using reusable code to save time and money while letting developers concentrate on other crucial aspects of application development. Fintech applications are practical in fields like credit risk that demand less human presence and lower the cost of having people serve customers since many procedures are automated.

Enhanced Customer Experience and Engagement

An organization’s competency and growth will increase using a fintech solution to streamline the investing procedure. Fintech may be used successfully and affordably to enhance the consumer experience. Using Big Data and Artificial Intelligence allows for more customized consumer experiences by suggesting services and goods based on prior purchases and financial position. In contrast, faster and more convenient service increases client retention.

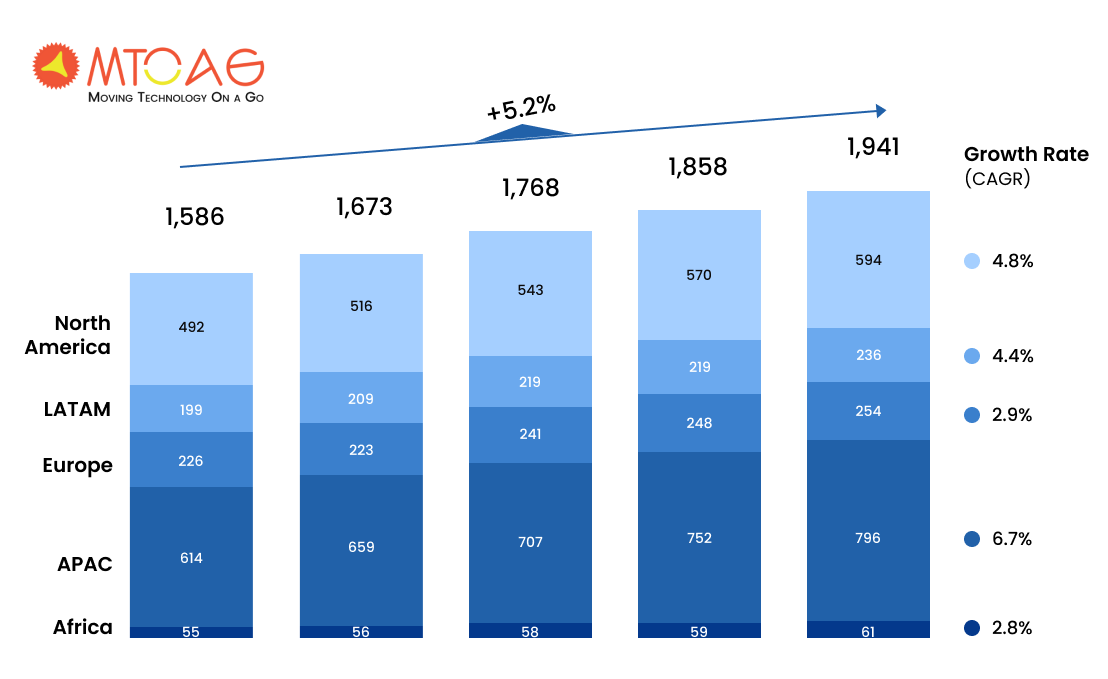

Compared to the worldwide average of 5.2%, Accenture’s internal predictions for the worldwide Payments Revenue indicate that APAC will have the highest payment growth, at 6.7% year over year. (Source: bankblog.Accenture)

Increased Revenue Opportunities

Despite being one of the most crucial corporate sectors, money is often handled worst. Fintech’s ability to streamline financial procedures is one of its more critical points. Thanks to digital banking systems, businesses can automate crucial financial processes and maintain their books more easily. Real-time transactions may be watched, updates come in real-time, and payments can be paid and received quickly. Moreover, controlled access is a feature offered by digital banks, allowing for the assignment of restricted capabilities to specific accounts.

Market Competitive Advantage

As fintech apps are designed to be mobile-first, they may help companies reach a large audience across various platforms, such as smartphones, tablets, and other mobile devices. Mobile applications are more practical for clients who like staying current on the news about their favorite businesses.

Fintech companies with mobile apps have a higher customer retention rate than those without one. (Source: The Financial Brand)

Benefits of Fintech Mobile Apps for Customers

Discussing the advantages of fintech mobile applications for users does not need any particular coding. Nonetheless, the followings are some illustrations and clarifications of the issue that arose in the query:

Greater Convenience and Accessibility

Customers using fintech mobile applications may access their financial data and conduct transactions anytime, anywhere, without going to a bank branch or using a computer. This saves time and effort and may be particularly helpful for those with hectic schedules or who reside far from city centers. Customers may, for instance, check their account balance, transfer money, pay their bills, or apply for a load from their smartphone using a mobile app.

87% of consumers say they would use a fintech mobile app if it offered needed services. (Source: KPMG)

Personalized Services and Recommendations

Fintech mobile applications may assess a customer’s financial behavior and preferences using data analytics and machine learning algorithms. They can then provide customized services and suggestions in line with those findings. For instance, a mobile app may provide notifications and reminders for approaching bills or payments or propose an appropriate investment strategy based on a customer’s risk tolerance and financial objectives. This may assist clients in making wiser financial choices and achieving their goals more quickly.

Improved Financial Literacy and Empowerment

Fintech mobile applications may also provide educational information and tools to assist users in improving their financial literacy and empower themselves to make wise choices. For instance, a mobile app may guide setting up a budget, saving money, investing, managing credit, or giving users access to financial calculators and simulators. Customers may feel more empowered to take charge of their money and create a better financial future.

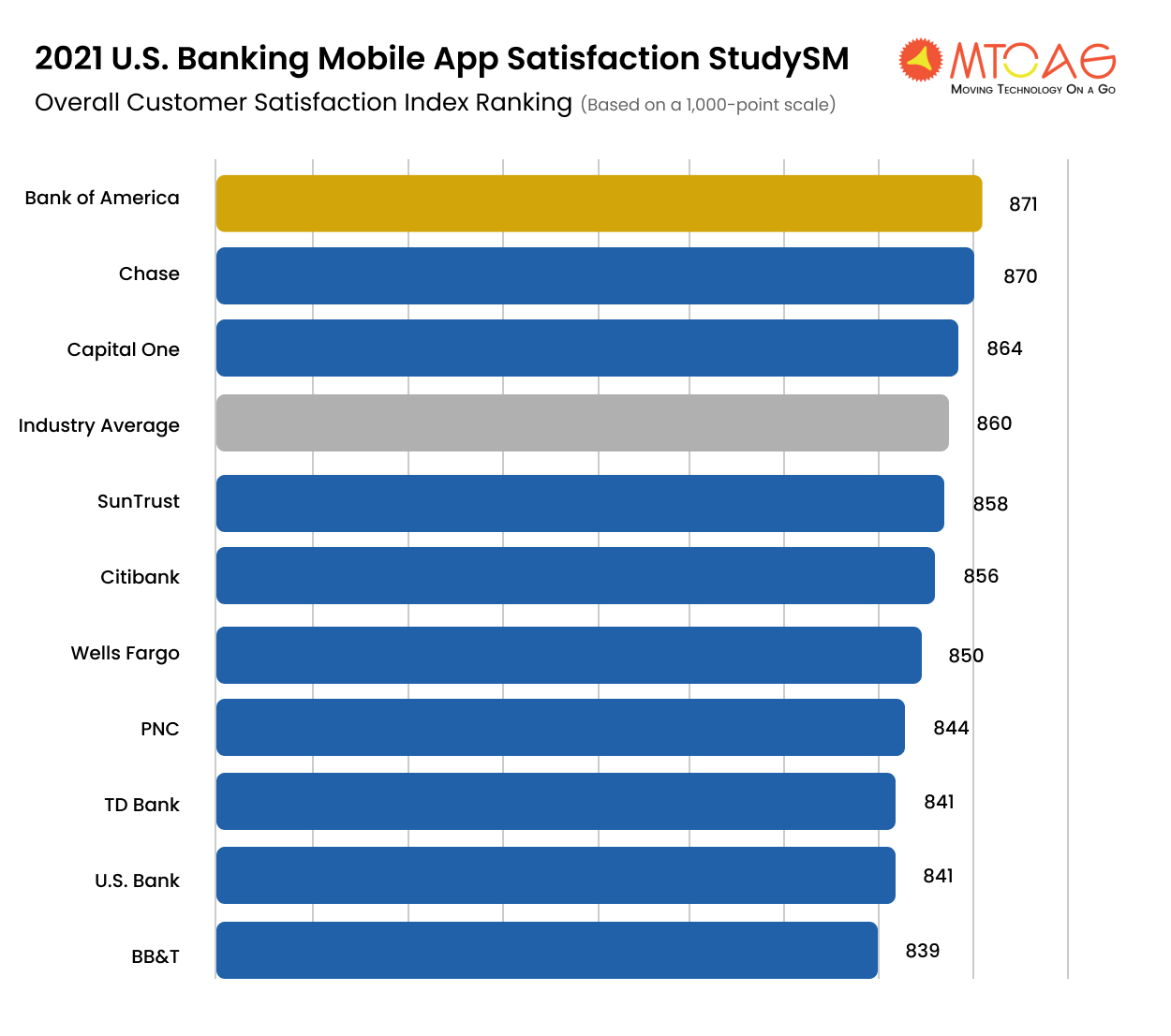

Bank of America ranks highest in banking mobile app satisfaction among national banks, scoring 871. Chase (870) ranks second, and Capital One (864) ranks third.

Why Outsource Mobile App Development to India?

Advantages of outsourcing to India (e.g., cost-effectiveness and skilled workforce)

1. Cost-Effectiveness

All of the justifications for outsourcing revolve around money. India has shown to be the most economical country. Compared to India, labor prices are astronomical in the U.S., U.K., Australia, Canada, Greece, and Dubai. Increased ROI is closely correlated with lower expenses.

Instead of recruiting internal staff, agencies outsource their operations to Indian firms that provide them with a committed workforce that will function just as the internal team would work for foreign agencies. In addition to flexibility, it significantly lowers capital investment, infrastructure, and maintenance expenses.

India has the world’s second-largest internet user base, with over 700 million users. (Source: Statista)

2. Skilled Workforce

Business outsourcing to India makes it easier to obtain knowledgeable and experienced people who have the greatest concentration of competent workers in industries like I.T., BPO, and finance, to mention a few.

India also claims the highest expertise in successfully managing complex projects. The cherry on top for the companies with offices overseas, among others, the U.S., U.K., Australia, Canada, and Dubai, is the availability of component labor at affordable prices.

The average cost of outsourcing app development to India is $30-$50 per hour, compared to $100-$150 per hour in the U.S. (Source: Clutch)

Leading Indian Mobile App Development Business

1. Mtoag

We are one of the leading mobile app development companies that offer the best fintech solutions. Also, it has left an influential mark on India’s finance industry. Mtoag has been serving its services since 2009 and has achieved a lot. Also, when he entered the fintech industry, it had been walking upward in a successful direction.

2. Eclair WebTech

Since 2011, eFlair Webtech has had no difficulties. One of India’s finest mobile app development firms, because of their client-centered approach to mobile app development, they have progressively expanded their customer base to include small and large businesses. One of their primary competitive advantages is knowing their clients’ demands and using schema design to create future-proof applications built to last the test of time. They are focused on correctness, timely deliverability, and outshining the competition in every way imaginable.

3. Zensar Technologies

The publicly listed Indian corporation Zensar Technologies strongly focuses on always prioritizing its client’s needs. The business works with customers from diverse backgrounds and industries, including those in banking, retail, high-tech manufacturing, education, and insurance. They have a wide range of products in their portfolio, including data engineering, analytics, and application services.

4. Infosys

Throughout time, Infosys has established a solid reputation in the market as a symbol of high-caliber services, dependable delivery, and expert client connections. This Indian mobile app development business services various sectors, including manufacturing, insurance, and finance. It also offers other I.T. services, such as digital transformation, third-party service integration, and consultancy.

5. TCS

TCS is well-known for its I.T. consulting services and works with some of the best app developers in the business. The firm has a long history of supporting many industries, including energy, I.T., engineering, consumer goods, chemicals, communications, and other fields. It also boasts a diversified portfolio of cutting-edge digital solutions.

Case Studies of Successful Fintech Mobile Apps in Greece

Examples of Greek fintech companies using mobile apps to disrupt the financial industry

A Greek fintech firm called Viva Wallet provides mobile payment options for companies. Businesses may collect payments from clients using their cell phones thanks to their mobile app. The app assists companies in tracking their sales and income and offers real-time statistics and analytics.

With an investment of €100 million in cash, J.P Morgan has bought a 48.5 percent share in the Greek Fintech Viva Wallet. Minority shareholders Hedosophia (24%) and the Latsis family (13%), as well as Deca (10%), approved the sale of their shares to J.P. Morgan before this.

The creators of Viva Wallet, Haris Karonis and Makis Antypas, still have a majority 51 percent interest and will continue to run the business.

The average cost of outsourcing app development to India is $30-$50 per hour, compared to $100-$150 per hour in the U.S. (Source: Clutch)

Description of the apps’ features and benefits

1. Mobility

If your phone can act as a card terminal, you can take payments wherever you are. For delivery drivers, couriers, and other types of independent contractors, for instance, it allows them to accept payments anywhere without having to carry around a card terminal. Every professional who wants to take payments on the move may use the Viva Wallet POS software, regardless of their line of work.

2. Hardware Independent

An app’s flexibility and adaptability are critical differences between utilizing a card terminal and the free Viva Wallet POS software. For instance, before you can restart operations, you will need to purchase a new card terminal if your conventional POS equipment is broken or stolen. But with the Viva Wallet POS software, you can quickly install the app on a different device, even if the smartphone you use to process payments unexpectedly stops operating.

3. Several Devices

For companies with various staff, having a variety of devices, they may use to take payments is now effortless thanks to the Viva Wallet POS software, which enables all Android smartphones and tablets to serve as card terminals. Employees can accept payments from anywhere in a business in this fashion, reducing strain on the cash registers and allowing for the accommodation of more customers without resulting in a crowded environment.

Success Metrics and User Feedback

With operations in 23 European nations, cloud-based Viva Wallet offers card acceptance services via its POS application, add-on Google Play devices, and cutting-edge payment methods in online retailers.

Takis Georgakopoulos, head of global payments at JP Morgan, said, “We are extremely happy to make a strategic investment in Viva Wallet to support their goal to unleash new growth and payments innovation focused at European small and medium enterprises.”

With more than 17 million retailers prepared to install payments systems that can be rapidly scaled up, he said that the European payments industry offers a significant amount of potential.

The minority owners of Viva Wallet, notably the Latsis family office, which owns about 13% of the company, and British fund Hedosophia, which owns approximately 24%, will sell their shares to purchase the holding.

The former Barclays CEO Bob Diamond and fellow Atlas Merchant Capital partner David Schamis controlled Greece’s first digital challenger Praxia Bank, which was acquired by Viva Wallet in 2020 after receiving a banking license.

It provided customers with digital business debit cards while Apple Pay and Google Pay were made available in 18 countries.

The co-founder and chief executive of Viva Wallet, Haris Karonis, stated: “Viva Wallet’s objective is to alter the way companies pay and get paid in Europe using cutting-edge technology.”

Viva Wallet’s legal and financial advisors on the transaction were Davis Polk & Wardwell LLP and Jefferies.

Conclusion

Recap of the benefits of fintech mobile apps for companies and customers

The demand for financial services is growing, making connecting with clients online more critical. This implies that in the current digital era, fintech applications are not only a crucial tool for companies wanting to increase income, but they can also help them remain ahead of the competition.

Fintech applications also contribute to greater financial inclusion by giving underbanked and underprivileged groups access to financial services. Blockchain and artificial intelligence are just two examples of cutting-edge technology that fintech firms use to lower obstacles and expand possibilities for individuals all around the globe.

The U.S. was followed by Asia and Europe in fintech investment – with $18.2 billion invested in U.S. fintech, compared to $8.2 billion and $5.6 billion in Asia and Europe, respectively. (Tech Crunch)

Final thoughts on the future of fintech in Greece

Greece’s fintech industry has a promising future, with room for expansion and innovation. While obstacles must be addressed, the public and commercial sectors collaborate to provide a favorable environment for fintech firms. There is an enormous opportunity for businesses to grow and assist neglected communities.

Call to action for companies to consider adopting fintech mobile apps for their business.

Fintech applications may provide businesses with several benefits. By providing convenience and accessibility, fintech applications may promote consumer loyalty and retention. They can also enhance the buying experience by integrating cashless mobile money systems into e-commerce apps. Additionally, by streamlining financial transactions and investment processes and offering analytics capabilities through automation, machine learning, and big data to identify irregular activities that may lead to fraud, fintech apps can help businesses improve their operational efficiency and revenue growth. Additionally, by offering online and real-time payments, enhancing the customer experience, and making it simpler to borrow money via digital loan applications, fintech apps assist companies in addressing many of the problems that customers have historically had managing their finances.

Given these advantages, businesses must think about implementing fintech mobile applications. Fintech usage was already increasing in 2019, as was noted on Forbes.com, but the adapt risk needs to be addressed as the bar for innovation keeps rising. According to spdload.com, the financial technology industry has a low barrier to entry, making it a fertile field for enterprises of all stripes to flourish. Using open banking APIs, non-banking companies may quickly build supplier agreements and deploy a functional product. Anyone may effectively own a successful outcome in this market if they have the necessary fintech product creation understanding.

The payments industry respondents believe they could lose up to 28% of their market share, while bankers estimate they are likely to lose 24%. All financial services sectors thought at least one-fifth of their business was at risk by 2020.

To profit from the many advantages that fintech mobile applications provide, firms should consider this. These applications may improve corporate operations, foster client loyalty, and open up many commercial prospects. According to ilounge.com, fintech applications may help organizations and customers with challenging business operations by offering cost-effective and efficient app solutions.

SWOT

Strengths:

- Fintech adoption may result in cost savings and enhanced income prospects for businesses.

- Fintech mobile applications provide more convenience and accessibility for clients.

- Greece’s fintech sector is expanding, and several profitable businesses exist, like Viva Wallet and Paylink.

Weaknesses:

- Fintech requires most of the investment and infrastructure changes for organizations.

- Customers who prefer conventional banking may be reluctant to trust digital financial services.

- Greece continues to have economic difficulties that may hinder the development and long-term viability of the fintech sector.

Opportunities:

- The Greek government has endorsed the fintech sector and may provide financial incentives to businesses that do so.

- Since so many people in Greece still use cash for the transaction, there is a sizable potential market for fintech services.

- The COVID-19 epidemic has hastened the transition to digital financial services and opened new business prospects for fintech firms.

Threats:

- Customers may be discouraged from adopting fintech services due to cybersecurity risks and data privacy issues.

- Fintech firms compete with conventional banks and other fintech startups.

- Regulation and compliance requirements changes may impact the development and success of fintech businesses.