Banks should embrace two key strategies in the face of fierce competition in the digital banking market: customer-centricity and mobile app innovation. A Citi Survey reveals that 80% of mobile banking customers with well-functioning applications are more likely to remain loyal to their service providers. This underscores the potential for banks to retain and attract customers through innovative mobile app features. The survey also warns that businesses that neglect mobile app capabilities risk losing out to their more innovative counterparts. Therefore, investing in features and updates that enhance the mobile banking client experience is not just a choice, but a necessity for finance app development.

The Insider Intelligence report confirms the pervasive role of mobile banking in everyday financial transactions. The increasing percentage of US account holders who prefer mobile banking over traditional methods like in-person branch visits or desktop software usage is a testament to this trend.

Financial institutions must not only adopt creative banking concepts but also prioritize customer-centricity to remain competitive, attract and retain customers, promote financial inclusion, and seize new international opportunities. This emphasis on customer-centricity is not just a trend, but a fundamental shift in the way banks operate, placing the customer at the heart of their digital banking strategies.

Table of Contents

Let’s delve into the history of m-banking to understand its evolution. The first iteration of m-banking in the 1990s used SMS. However, in 1999, with the introduction of the mobile web and cellphones equipped with wireless access protocol (WAP), European banks took a leap forward by providing their customers with m-banking platforms. This marked a significant shift in the landscape of mobile banking technology.

Before 2010, banks provided banking services on their customers’ mobile devices using SMS and the mobile web. However, in 2010, the emergence of the subsequent elements totally transformed mobile banking:

Apple and Google are developing iOS and Android, respectively, for smartphones.

The emergence of web-based technologies (WBT) such as HTML 5, CSS3, and JavaScript made it possible for banks to build mobile and online apps for Android and Apple devices. Consequently, banks began adding sophisticated capabilities to their applications in an effort to attract users. Customers were lured in by the easily accessible applications’ improved usefulness. As a result, these mobile banking applications have become the new standard everywhere over time.

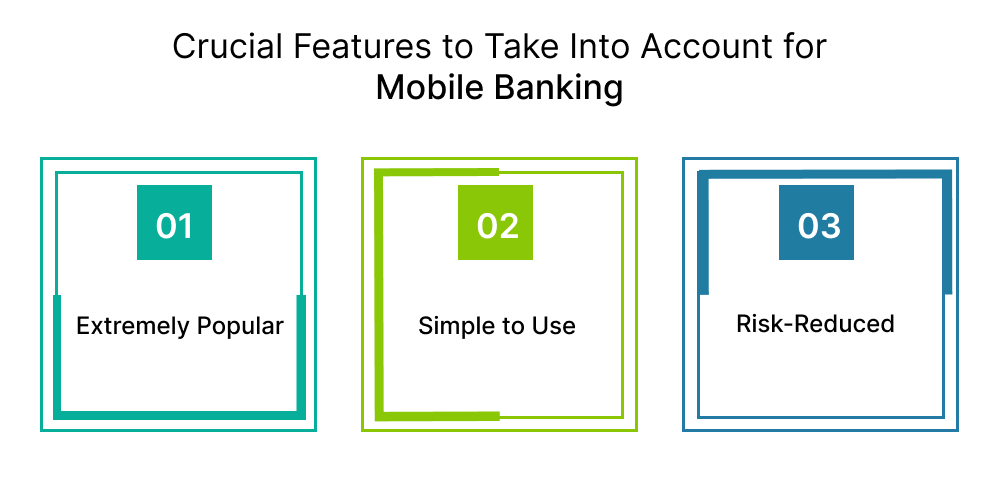

Crucial Features to Take Into Account for Mobile Banking

Although banks have the option to include several features in their mobile applications, not all of them are appropriate. Service providers should carefully consider the needs of the market and compile a short list of features for mobile banking, such as:

Extremely Popular:

Depending on where your target market is located, some mobile banking services are more popular with clients than others. Banks and other financial institutions should give top priority to features that meet client expectations and will likely be in high demand in the future.

Simple to Use:

You have a brief window of time, among the many mobile banking applications, to capture users’ interest and hold it on your offering. By focusing on features that can be utilized with a few clicks, banks may enhance the client experience while reducing the amount of work they have to do when providing instructions.

Risk-Reduced:

Banking services require strict, sometimes intricate management procedures that include database and technology management, security, legal compliance, and other areas. It is crucial to verify that the features can lower fraud and maintain the security of user data.

Creative Elements for a Mobile Banking App Technology

Financial institutions must not only incorporate essential features into their mobile apps but also stay abreast of the latest advancements in the mobile app development industry. This is crucial as the majority of clients use these apps for their everyday financial transactions. By maintaining high standards for their services and offering additional services, financial institutions can expand their client base and tap into new income streams.

The cutting-edge features listed below can be quickly and easily added to digital banking systems.

Want to Hire Website developers for your Project ?

1. The Use of Secure Authentication

According to Verizon’s study on a data breach investigation, 86% of cybercrimes are committed with the intention of stealing money, and fraudsters often target mobile banking applications. In light of this, service providers must focus more on security features – like multi-factor authentication –during app registration or onboarding. This identity verification procedure, which often entails several processes, must be quick, easy, and safe. The most common authentication methods in a lot of applications include message confirmation, encrypted PINs, and one-time passwords (OTPs).

Mobile banking development companies have progressively included biometric authentication in their applications. This confirms users based on their bodily attributes, such as face, fingerprints, voice, and others, to safeguard accounts and devices from unwanted access. Wells Fargo Bank may enhance user security by investing in eye-scanning equipment, which can identify distinctive characteristics like blood vessels.

Moreover, electronic know-your-customer (eKYC) with biometric selfie verification is rapidly gaining traction as a way to strike a balance between security and user experience throughout the onboarding process. This technology aids in the digitalization of the manual KYC procedure in digital banking and guards against identity theft.

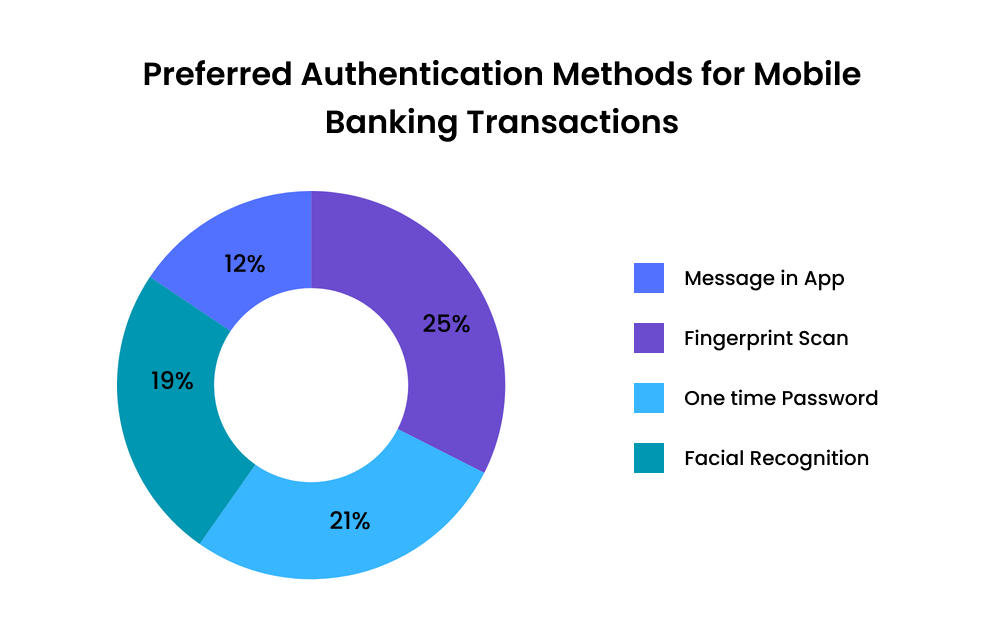

90% percent of individuals surveyed said they prefer to use their phone to verify a transaction before completing it. They listed the several forms of verification that their banks use to confirm transactions: 25% utilize a fingerprint scan, 21% a text-received one-time password or code, 19% face recognition, and 12% message their banking app to confirm.

One other crucial element for banking apps to enhance user experience is biometric authentication.

2. Payments using QR Codes

Nowadays, various sectors, including banking and retail, are adopting this black-and-white square, which is very popular since it enables customers to make contactless payments more quickly. Customers may make purchases without using bank cards by utilizing a QR code. With this function, verifying payment and scanning the code with your data safely encrypted takes a few seconds.

According to recent QR payment studies carried out in China, one-third of the population already uses QR codes for everyday purchases. Between 2020 and 2024, the number of QR code transactions is predicted to increase by 16.4%. Additionally, as merchants and eateries print or provide QR codes on every slip and bill, this practice is said to have extended across the Asia Pacific area in Singapore. This allows visitors to quickly scan the code and make payments in their native currency.

Want to Mobile App Development for your Project ?

3. Chatbots Driven by AI

Regardless of the sector, customer service is a crucial element affecting loyalty. Banks and other financial organizations should consider offering round-the-clock help to improve service availability and personalization of banking applications. They can handle many incoming queries at once by using conversational technologies, including the Chatbot function, which cuts response times from hours to seconds.

Artificial intelligence (AI)-driven chatbots may mimic human responses, including real-time customer support, tracking recurrent problems, and offering a customized experience. Additionally, since this functionality serves users in several languages at all times, it enhances the customer experience. Banks may also consider using algorithms and consumer data analysis to tackle more complex instances. This kind of deployment makes better competitiveness against challenger banks possible, which might be crucial to the digital transformation process.

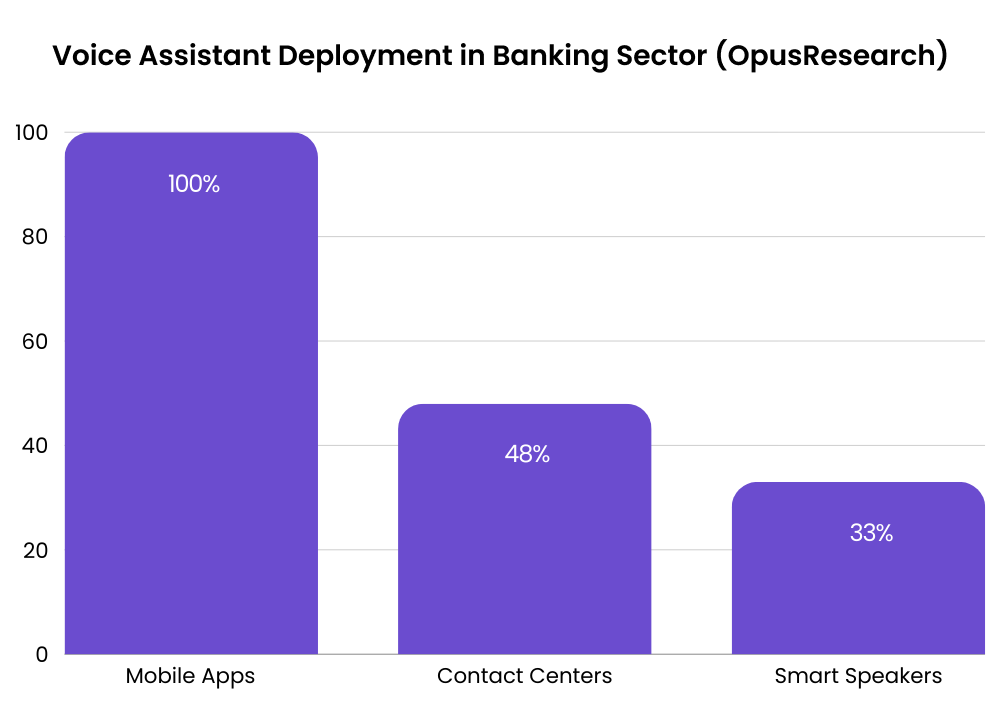

4. Virtual Assistants with Voice Activation

It’s clear that using digital assistants is becoming more popular. 75% of iPhone users and 63% of Android users have spoken with virtual assistants on their cell phones.

Grand View Research projects that the global voice-based payments industry will expand at a compound annual growth rate (CAGR) of 10.9% between 2022 and 2030. By focusing on voice-based transaction capabilities, banks, and other financial institutions can set the pace for the industry and enhance the client experience.

Using this touchless payment capability, users may instruct the virtual assistant to pay their bills or complete a specific transaction. In keeping with this trend, Bank of America has created Erica, a virtual assistant that makes it simple to check account balances and make transactions using voice commands.

Since many clients are already used to this technology, phone banking is only their subsequent logical development. By using these cutting-edge features, banks may increase the total value of their brand and establish a strong relationship with their other mobile banking services.

5. ATM Withdrawal without a Card

Cardless ATM withdrawal is one of the tremendous mobile-based branchless banking solutions that will be popular in 2021 and the years to follow. Thanks to advancements in NFC technology and QR code scanning, users may now effortlessly use their mobile phones to interact with banking ATMs. Customers may use this function in the mobile banking app to take cash out of the ATM and make contactless payments without using their cards.

Various bank strategies may dictate a different implementation of this functionality. The following are some of the cardless ATM withdrawal choices that various banks provide:

Customers using Commonwealth Back’s cardless ATM withdrawal service must first submit and validate their transaction amount online to get a transaction code, which they must then input into the ATM to withdraw cash.

Wells Fargo Bank’s app offers a unique card-free access function. It uses NFC technology to read card information via a symbol in mobile applications. Users must first transfer money from their bank account to their digital wallet.

6. Financial Administration

Investing is one option available to those who are looking for passive income sources other than their salary today. Given this growing need, investment services might be introduced as a value-added feature to mobile banking applications. Since many people now have easy access to investments in stocks, exchange-traded funds (ETFs), real estate, and cryptocurrencies, it is possible to enable the acquisition and administration of assets via a popular novel banking concept for several service providers.

Using the investment management function, customers may manage their portfolios or get real-time information. In this way, customers need to touch their phones a few times to invest in the securities they choose.

7. Depositing Checks Online

Traditional branches are becoming less and less common. Mobile banking applications have already replaced some services offered in physical locations, although not all can be completed online. While some American and European banks have added this functionality to their mobile banking applications, other areas still need to see it deployed. In light of the growing demand for these services in the Asia-Pacific region, online mobile check deposits have just been accessible digitally.

Customers may scan their checks using a mobile camera and a portable scanner in the banking app to employ OCR (Optical Character Recognition) technology. They can then send the papers to the banks with a digital picture and recognized text. The user may save time by not having to visit branches to do this straightforward job since the deposit data is sent straight to their account.

Ready to bring your B2B portal or app idea to life?

8. Systems of Peer-to-Peer Payments

Peer-to-peer, or P2P, payments are made possible by internet technology that enables users to transfer money directly to another individual from their bank account or credit card.

According to Jim Marous’ Digital Payment Report, the general population is starting to use mobile payment solutions. If the banking sector hopes to retain its tech-savvy clientele, it will have to adjust to emerging trends in mobile payments.

P2P payments are still one of the best ways to maintain user involvement, even if they have never been about making money. In an effort to enhance consumer satisfaction and explore novel avenues, such as peer-to-peer payments, the companies are investing more in payment systems.

Peer-to-peer payments enable consumers to send and receive money directly using only an app. The consumer gains some freedom from not having to rely on a more extensive organization to conduct money transfers since it’s almost an instantaneous transaction (although moving the money to a bank account may take a few days).

By adopting this technology, PayPal has controlled the industry for almost a decade. Still, an increasing number of banks and credit card firms are now open to adopting person-to-person payments.

9. Recognition of Images

Upon joining Radius Bank in 2008, Mike Butler was presented with two choices: either adhere to the standard growth model and establish physical banking branches or prioritize allocating the bank’s resources towards the mobile channel.

It was an easy option for him. In a matter of years, Radius Bank went from having six physical locations to only one.

Few in 2008 could have predicted that mobile banking would become so popular by now. Thus, this drastic strategy of becoming completely digital needed a blend of cutting-edge technology and user-friendly solutions.

Chris Tremont, EVP of Virtual Banking at Radius, states that understanding what their consumers want and working out how to produce and deliver it is the cornerstone of Radius’ approach.

For instance, they were excellent the first to include picture recognition into their brand-new mobile banking app feature.

To create an account, a client must take a photo of their driver’s license and submit it to the banking app. They no longer need to visit an actual bank branch.

10. Advanced Analytics and Big Data

Financial and banking institutions serve millions of consumers, making them the most data-intensive businesses in the world economy.

In digital banking competition, the banks that can consistently provide their clients with individualized offers and experience will emerge victorious.

The mountains of data across various banking channels hold the key to comprehending what clients want and need.

Banks can only really listen to their consumers and provide tailored financial services that will help them by evaluating data.

Banks have access to a wide range of data sources, including payments made online and via mobile devices, ATM withdrawals, use of digital banking channels (mobile app, internet banking, e-wallet), Internet of things devices, client information gathered for KYC, biometric identification, etc.

Concluding Remarks

Banks and credit unions often consider what features they already have or would need to add to their mobile app in order to increase earnings. Nonetheless, the banking sector now prioritizes client retention and care due to the ongoing shifts in people’s needs.

By incorporating these cutting-edge banking services, you may enhance your competitive advantages and client satisfaction, which will increase loyalty and sales.