Technology has permeated every area of our lives in the modern day, and the financial industry is no different. Fintech, or financial technology, has grown significantly in the last ten years. Let’s examine the Fintech trends that have emerged in India in recent years and predict the sector’s future.

Following the 2016 Demonetization and the advent of a cashless economy, several companies entered the market, increasing the share of digital payments from 10% to 20% of total transactions and establishing new Fintech trends in India. Table of Contents

According to BSFI, India has the highest Fintech adoption rate globally, at 87%, whereas the average rate worldwide is 64%. The COVID-19 outbreak largely fueled these developments in the Fintech sector. However, in their daily lives, consumers have accepted and adjusted to these financial tendencies.

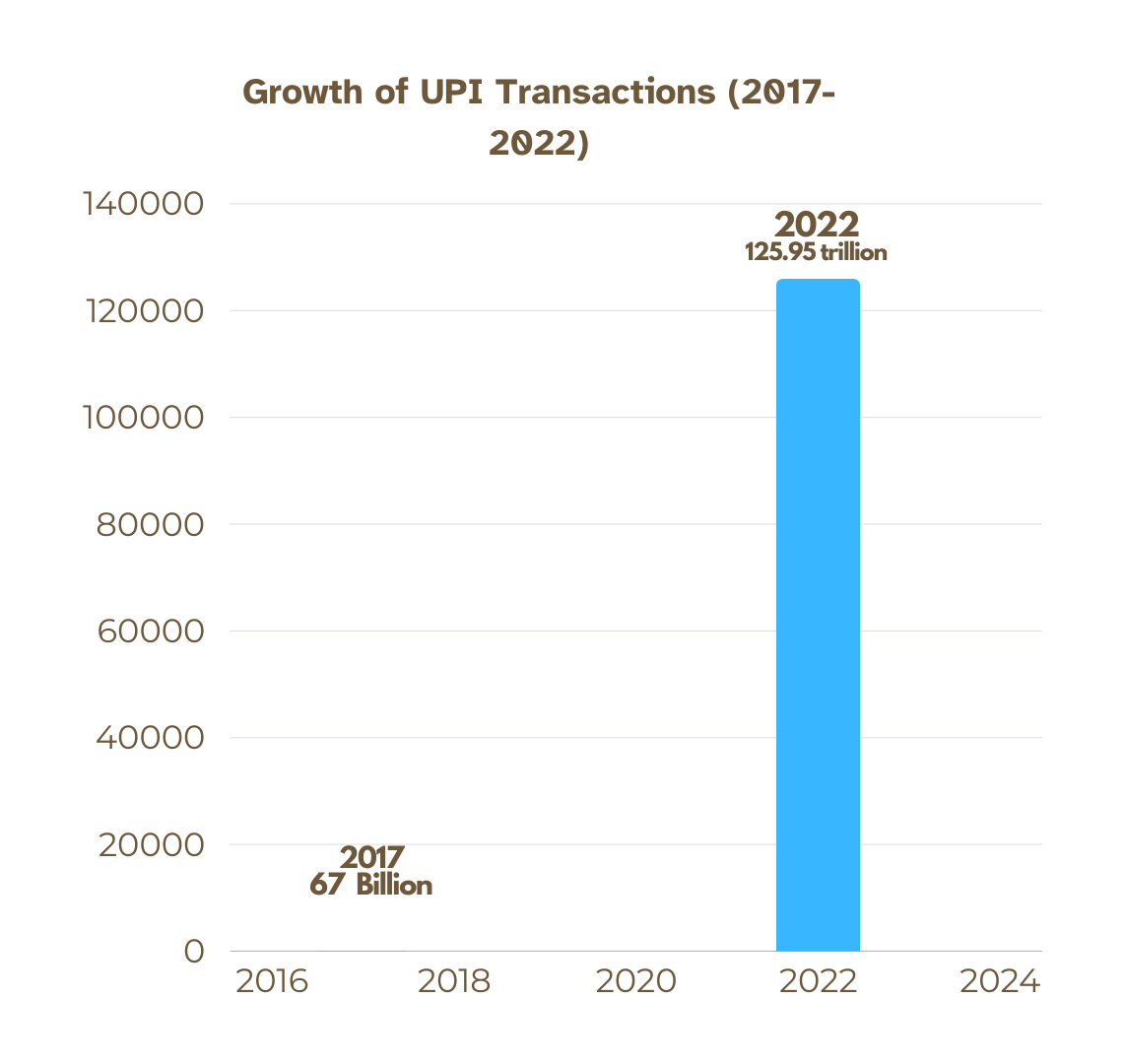

Over 100 million transactions of INR 67 billion were conducted using UPI in 2017. By the end of 2022, that amount had risen to INR 125.95 trillion. (Refer to NIC) (squadstack)

Furthermore, these numbers provide a glimpse into India’s payment market. FinTech businesses now have a larger market share and are predicted to grow at a compound annual growth rate (CAGR) above 10%.

Market Insights and Forecasts for Fintech Startups and Innovations

Globally, there are over 26,000 fintech companies, substantially growing over the last few years (from just around 12,000 fintech startups in 2019).

Market insights and estimates show that the fintech industry is expanding substantially. Revenues in this sector are expected to expand almost three times faster than those in conventional banking.

Technological advancement, creativity, and the incorporation of cutting-edge technologies like blockchain, artificial intelligence (AI), robotic process automation (RPA), and application programming interface (API) are what are driving this expansion.

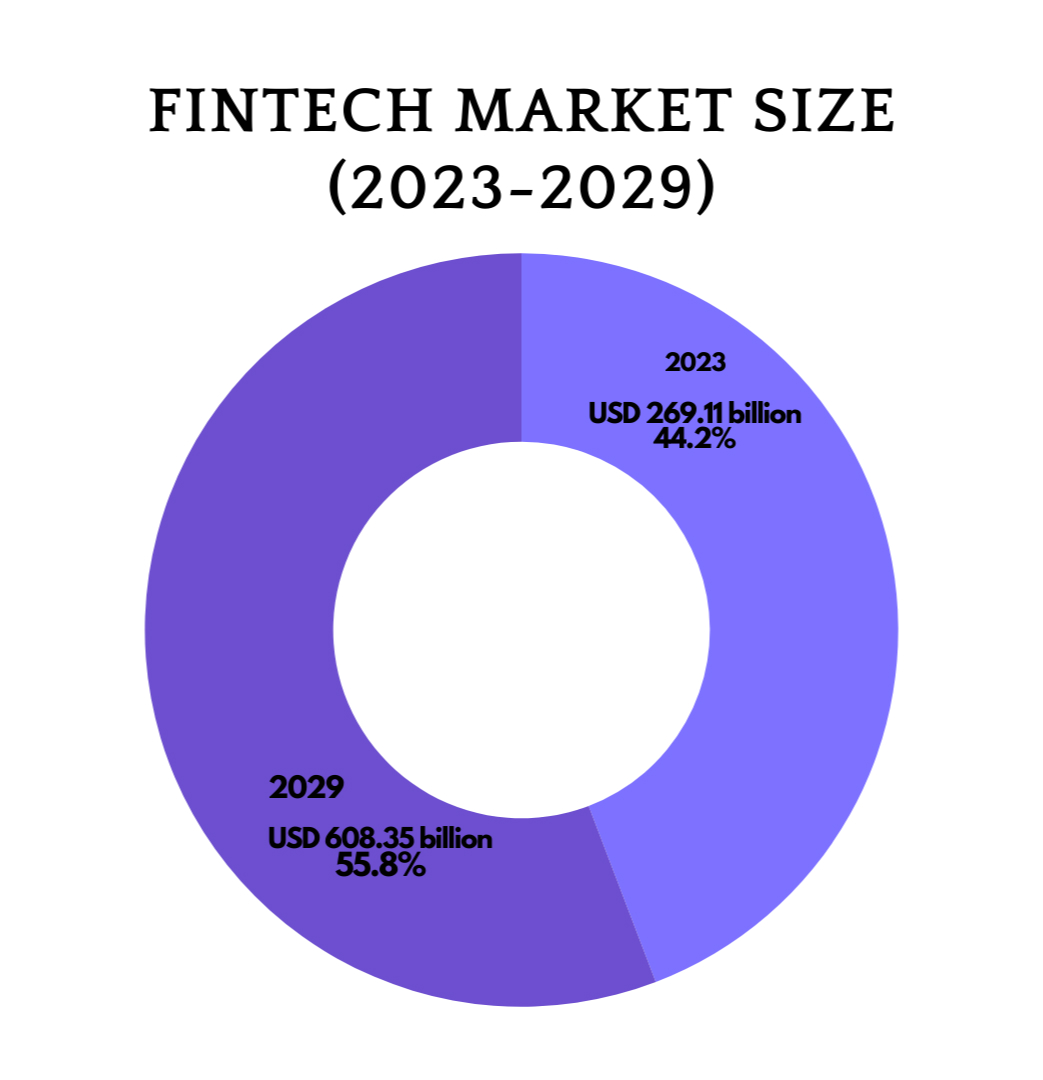

The worldwide Fintech industry is expected to grow at a compound annual growth rate (CAGR) of more than 14% over the forecast period, from an anticipated USD 269.11 billion in 2023 to USD 608.35 billion by 2029. (marketsandmarkets)

North America has the most significant market share, with the Asia Pacific region predicted to develop at the quickest rate.

Technological advancements in cloud computing, blockchain, AI, RPA, and machine learning shape the fintech industry.

These innovations improve data security, financial services customization, fraud detection, and customer support.

However, worries over data security and privacy might hinder business expansion.

PayPal, Mastercard, Fiserv, Block, Rapyd, Envestnet, Upstart, Solid Financial Technologies, FIS, Synctera, Stripe, Adyen, Dwolla, Finastra, Revolut, NIUM, Airwallex, SoFi, Marqeta, Finix, and Synapse are a few of the major competitors in the fintech business.

These businesses provide various financial services, including blockchain technology, peer-to-peer lending platforms, fraud detection, and payment processing.

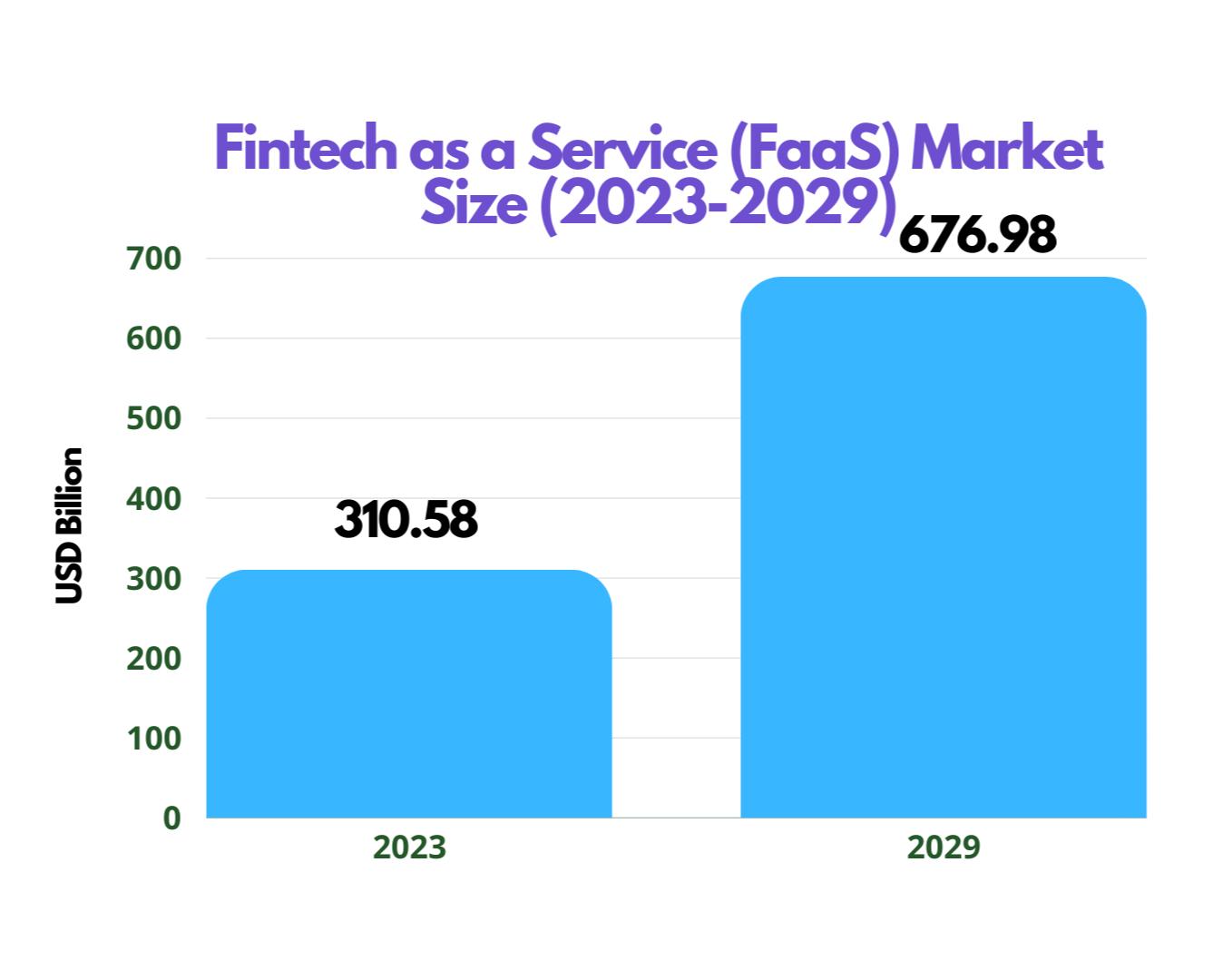

The Fintech as a service (FaaS) industry is expanding significantly as well; estimates place it at USD 310.5 billion in 2023 and USD 676.9 billion by 2029, with a compound annual growth rate (CAGR) of 15.9% over the course of the projected period. (marketsandmarkets)

FaaS is a cloud-based platform that gives companies access to various financial services, including lending, investing, and payments. By eliminating the need for them to create and manage their own financial infrastructure, businesses can save money and time.

In conclusion, the Fintech industry is expanding rapidly due to technological advancements, shifting customer preferences, and new laws. The industry has a lot of room to grow, but there are issues with trust, security, and data privacy. The industry is being shaped by significant technological advancements in cloud computing, blockchain, AI, RPA, API and machine learning, PayPal, Mastercard, Fishery, Block, Rapyd, Envestnet, Upstart, Solid Financial technology, FIS, Synctera, Stripe, Adyen, Dwollaa, Finastra, Revolut, NiUM, Airwallex, SoFi, Margeta, Finix, and Synapse are a few of the prominent companies in the Fintech industry. FaaS is a rapidly expanding sector that provides cloud-based platforms for companies to access various financial services.

Impact of Regulatory Changes and Technological Advancements on the Fintech Landscape

The dynamic Fintech sector is seeing a shift in the landscape and direction of innovation due to regulatory developments. The intersection of technology and finance is undergoing significant transformation, and regulatory bodies are adapting to match the swiftly shifting dynamics of the digital finance domain. The regulatory landscape significantly impacts how financial technology is altering traditional banking and payment systems, and it may either support or impede the growth of Fintech businesses. Regulation changes have a significant effect on the FIntech sector. Governments and authorities worldwide are constantly upgrading and revising their regulatory frameworks to keep up with the fast changes in the Fintech industry.

In recent years, the fintech industry in India has experienced a notable rise, as well-established firms and creative startups have reinvented the provision of financial services. Consumers have benefited greatly from this wave of FIntech adoption, which has increased the accessibility, effectiveness, and affordability of financial services. However, fast expansion also needs appropriate regulation and control.

Want to Hire Website developers for your Project ?

The Indian government has proactively acted to regulate the Fintech sector to guarantee consumer security and protection and promote ongoing innovation. These measures include various industry areas, such as digital lending, insurance technologies, payment systems, etc. The government hopes to foster an atmosphere that fosters Fintech businesses’ growth while safeguarding the financial security of the Indian populace by Finding a balance between innovation and regulation.

This strategy promotes a robust and long-lasting Fintech ecosystem in the nation while also protecting consumers, all of which help boost the country’s GDP. The government implemented many new regulation amendments in 2023, such as:

Framework for Regulatory Sandbox

To encourage innovation in the securities industry, the Securities and Exchange Board of India (SEBI) unveiled a regulatory sandbox framework in 2020. Under SEBI’s guidance, this framework enables Fintech businesses to test innovative goods and services in a monitored setting.

Draft Cryptocurrency and Regulation of Official Digital Currency Bill, 2021

This bill would outlaw all private cryptocurrencies in India and provide the foundation for an official digital currency to be issued by the Reserve Bank of India (RBI).

The Digital Personal Data Protection Bill of 2022 would provide a framework for safeguarding personal information, mainly that which is gathered by fintech businesses.

Want to Mobile App Development for your Project ?

Rules for Digital Lending

To shield customers from unscrupulous lending practices, the Reserve Bank of India (RBI) released rules for digital lending in 2022. These regulations mandate that digital lenders adhere to several standards, including upfront disclosure of all fees, provision of sufficient client protection measures, and fair and open debt collection procedures.

2022 Revised Master Directions on Credit Card and Debit Card Issuance and Conduct

In 2022, the RBI released updated master directions on the issuance and conduct of credit and debit cards. These guidelines seek to improve consumer safety and encourage ethical behavior in the debit and credit card sectors.

Explanation of the RBI’s previous master directions on prepaid payment instruments (PPI-MD)

The RBI released a clarification of its previous PPI-MD master instructions in 2022. Due to this clarification, PPI issuers are not permitted to load PPIs straight from credit lines.

The Payment and Settlement Systems Act (Amendment) Bill, 2023:

It would give the RBI further authority to oversee payment systems and combat fraudulent activities.

In addition to the aforementioned regulatory adjustments, the RBI and SEBI have implemented various additional measures to encourage innovation and safeguard consumers in the fintech industry.

Actions made by RBI:

- Establish a Reserve Bank Innovation Hub and a fintech department to encourage innovation in the financial industry.

- They established a regulatory sandbox structure to enable fintech businesses to test their goods and services under supervision.

- Launched many digital payment programs, including Aadhaar Pay and UPI.

- Published rules for online data security and digital lending.

Actions made by SEBI:

- We have published consultation papers on a range of fintech goods and services, including cryptocurrency and platforms for fractional ownership.

- Form a committee to investigate the viability of implementing a digital currency issued by the central bank (CBDC).

- We have established a regulatory sandbox specifically for fintech firms.

- We have published recommendations for the securities market’s usage of blockchain technology and artificial intelligence.

To create a welcoming environment for fintech innovation, the RBI and SEBI have been collaborating closely with various stakeholders, including the government and business community, in the following ways:

Getting Involved with the Government

The RBI and SEBI have collaborated with the government to create a regulatory framework supporting Fintech. This entails supporting regulatory requirement simplification and streamlining, tax reductions, and other incentives for financial businesses.

Working Together

The fintech sector has been working with the RBI and SEBI to create best practices and standards. To this end, rules on data security, consumer protection, and responsible innovation will be developed in collaboration with industry groups.

Ready to bring your B2B portal or app idea to life?

Raising Consumer and Business Knowledge about Fintech

The RBI and SEBI have been working to raise consumer and business knowledge about Fintech. This involves interacting with the media, holding workshops and seminars, and producing instructional materials.

These regulatory reforms will significantly impact the fintech industry in India. Therefore, regulatory improvements in India’s fintech industry are imperative to safeguard customers and foster innovation. It’s crucial to watch out for the rules to maintain creativity and avoid becoming too demanding. To ensure that the laws are just and balanced, the government must collaborate with fintech businesses.

Emerging Opportunities and Challenges for Fintech Entrepreneurs

Angel investing and fintech startups are quickly changing industries with a wide range of investment possibilities and hazards to consider. Prospective investors must evaluate the possible rewards and related risks before making any investment choices. We will review some important information and points to consider regarding hazards and investment potential in the Fintech sector here.

Market Growth Potential

Recent technological breakthroughs and shifting consumer habits have propelled the Fintech sector’s notable expansion. Startups have shown promising development potential in industries such as peer-to-peer lending, robo-advisory, blockchain, and digital payments. Investors may profit from this growth by finding firms with a strong market presence and creative solutions.

Regulatory Obstacles

Because financial services are so complicated, Fintech businesses often encounter regulatory obstacles. For companies to function lawfully and win over investors, compliance with laws pertaining to consumer protection, anti-money laundering, and data privacy is essential. Investors must examine the regulatory environment closely and consider how companies handle these difficulties.

Competitive Environment

Many companies are fighting for market share in the fiercely competitive fintech sector. Investors must evaluate each startup’s value proposition while examining the competitive environment. Startups having a competitive edge-like in-house technology, well-established clientele, or strategic alliances –might make for compelling investment prospects.

Technical Risks

Fintech firms mainly depend on technical infrastructure to provide their services. Investors need to assess how stable and scalable the technological platform businesses use is. Furthermore, cybersecurity risks and the possibility of data breaches should be considered, as they can seriously harm a startup’s brand and financial stability.

Financing and Exit Opportunities

Investors need to evaluate the financing alternatives accessible to fintech enterprises. Businesses with investments from respectable angel or venture capital companies may be more credible and have more potential for expansion in the future. Investors should also consider possible exit strategies that provide a return on investment, such as acquisitions or initial public offers (IPOs).

Customer Adoption and Retention

These two factors are critical to the success of financial firms. Investors want to know about the startup’s user experience, customer satisfaction scores, and methods for acquiring new customers. Entrepreneurs who exhibit a robust clientele and elevated rates of customer retention might potentially provide appealing prospects for investment.

Economic and Market Aspects

Aside from specific Fintech sector effects, investors should also consider wider economic and market aspects. Fintech firms’ development and profitability may be influenced by several factors, including, but not limited to, interest rates, economic stability, and regulatory changes. Evaluating these elements may assist investors in making wise financial choices.

Expert Interviews and Perspectives on Fintech Industry Trends

As a firm that offers development teams, among other kinds of teams, to FIntech organizations, we have chosen to interview one of our best subject matter experts on the subject of current and very pertinent issues: Fintech industry trends. We are presenting Yuriy B., a seasoned expert with a solid accounting and financial analysis foundation who is presently working on a well-known payment orchestration platform project for one of our clients.

These are the questions we should ask an expert to get their thoughts on current developments in the Fintech sector.

What Effects Has the Pandemic Had on the Fintech Industry’s Trends?

Naturally, the pandemic has had a significant influence on trends in the Fintech business and the overall economy, primarily individuals relocating from workplaces. Nonetheless, we think that since it created new opportunities, this change has been beneficial to the FinTech sector as a whole. People began to use mobile devices more often. A growing number of organizations started using the internet and cloud computing. While unrelated to the epidemic, this is undoubtedly a contributing element. Because more people are now paying attention to technology, this change has benefitted it.

Has the Pandemic Led to the Emergence of any Particular Tendencies in the Fintech Sector?

While the pandemic has positively impacted the field’s overall prospects for growth, we would not attribute any particular Fintech business developments to it. We can attest from our experience that more individuals are experimenting with financial instruments. That’s just our opinion. It’s more about individuals gambling like they’re in a casino than it is about purchasing choices or tangible goods. While some see it as a sophisticated trend in the Fintech business, it simply involves speculating on the rise of certain assets, such as currencies. As a result, many gamblers switched from wagering at casinos and on sports to financial gambling.

Which Fintech Technological Innovations Do You Believe Are Most Prominent at the Moment, and How Are They Influencing the Sector?

We are aware of the current programming developments in Fintech technology. In essence, everyone is attempting to migrate to microservices. What impact does this have on the trends in the Fintech industry? It’s hard to determine. Without a doubt, the need for fresh expertise grows as new technologies are developed. The need for assistance and integration of different systems available on the market has caused the pay of DevOps professionals to soar. This has affected the need for experts with integrative abilities. Software engineering hasn’t precisely been neglected; instead, it is mainly necessary for professionals to acquire new integration and support-related knowledge and skills in new technologies.

Which Technological Advancements Are Leading the Way in Fintech Today? Which one Will Shape Fintech’s Future the Most?

It is difficult to predict how technology will develop in the future. Trends in the Fintech sector are usually followed by technologies, not the other way around. Choosing technology is a constant. Microservices are thus one of the leading Fintech themes, as we have already shown. AWS and Kubernetes are the two microservice platforms we have experience with. Since we work only with Java, We are in a minimal position to comment on which programming languages are now top trends in Fintech. However, Java is very well-liked when paired with a standard set of technologies. For instance, Spring was unpopular in the US and Australia 10 years ago. However, the lightweight Spring has taken the role of EGB in recent years.

What Part Do You Think the Fintech Industry’s Current Trend of Artificial Intelligence Will Play in the Field’s Future?

While we lean toward the conventional understanding of this technology, artificial intelligence (AI) is undoubtedly a significant trend in Fintech. AI will not take the place of people in more complex areas of human endeavor. But it will be able to do so in little ways. AI can do our primary tasks. Many individuals desire to earn money in the Fintech business, but they will ultimately lose money. People play by particular rules when they use financial instruments. For AI to play financial instruments and make more money, people will feed the AI those rules and let the AI access their deposits. However, we are not sure that this approach will be financially successful. We are more confident that although it could provide some favorable outcomes initially, it won’t save them from losing in the long run. After all, investing in the stock market increases your risk of losing money.

What Role Will Blockchain Play in the Development of Fintech, and How Has the Adoption of Blockchain Technology Affected Trends in the Fintech Business in 2023 and Beyond?

Although we have yet to work with blockchain, we know that cryptocurrencies will be a convenient means of transmission of money in 2023. Therefore, this may be considered a trend in the Fintech sector. However, the market has significantly overvalued cryptocurrencies. Bitcoin is overpriced and has little real value. Second, we believe that bitcoin is being marketed to avoid taxes, and in the future, authorities will be closely monitoring it. Regulators aren’t getting involved right now because Bitcoin is profitable. But the bust of this bubble will cause a financial shock sometime in the next ten years or so.

Conclusion

Consumers are the actual driver behind all the fintech developments shaping the sector. Fintech has reached this point in its development due to its emphasis on providing customers with services they have never received before. These patterns show how customer tastes change and how Fintech may adapt to suit those demands.

Being adaptable to suit changing customer requirements and being abreast of consumer-driven trends is the most excellent approach for fintech firms to remain relevant and provide space for expansion.